Tera Studio & Pilates Club is barely a year old, but it's already harder to get into than New York mainstay hotspots like Torrisi and Carbonne.

Its address in New York's SoHo neighborhood is a closely-guarded secret. (Its distinctive red front door, which pops up on Instagram for those in the know, offers a clue.) The only way in is through a direct referral from one of its 300 members.

But Tera, where a 55-minute class costs $65, is selling more than exclusivity. "With the referral, we're almost filtering our clientele to be somewhat of the same person," says Georgia Wood Murphy, Tera's founder. By that, she means someone "that wants to invest in wellness, that wants to be on trend, and a part of what's hot in New York right now."

Corrie Aune for BI

Murphy, who previously taught at Forma Pilates, the celebrity-beloved studio that Vogue christened "Los Angeles and New York's most exclusive exercise class," says the referral model allows her to keep classes to around six people and get to know everyone personally. She follows all of Tera's clients on Instagram. "I'm super interested in where they went to dinner Friday, because I probably want to go there as well," she says.

For an elite few, working out at an exclusive, invite-only studio is the latest chapter in Gen Z and millennials' obsession with the gym.

Gen Z, the swolest generation, has been flocking to gyms to lift weights and make friends. Along with millennials, they make up more than 80% of gymgoers. But this influx has meant that gyms are getting crowded, with members queuing up for a squat rack at the gym or dodging limbs in a packed class.

Now, more than a great workout, zoomers and millennials are looking for exclusive fitness communities with like-minded members who are serious about their workouts and willing to pay a premium for a more bespoke experience.

Corrie Aune for BI

And these studios take the job of curating their membership seriously. "Would you post flyers on the street to invite someone to a dinner party at your house?" says Colette Dong, co-founder of the trampoline-fitness studio the Ness, which vets members before they're allowed to purchase a membership. "You wouldn't. You would curate the vibe."

Alice Berman, a 33-year-old novelist and a longtime client of Wood Murphy's, is among Tera's chosen few.

She works out at the studio seven days a week and appreciates that she can get into any class she wants.

The referral requests flooding Berman's Instagram DMs are proof of Tera's success. "Why is your Pilates place the hardest private members club to get into in New York right now?" one message read. There are currently 150 people on the waitlist, and an untold number of friends and strangers hitting up members in their DMs.

Corrie Aune for BI

But Berman is ambivalent about being a Tera ambassador: she says she's referred just one person. "It sounds bad, but it's hard enough to get one of six spots in an 8 a.m. or 9 a.m. class," she says. "I can't be competing with more people."

It's the same logic she applies to the two other Manhattan clubs where she's a member, Casa Cipriani and Chez Margaux, which has a restaurant run by Michelin-starred chef Jean-Georges Vongerichten. "It's not about feeling special because you're a member," she said. "It's about actually enjoying a really good Pilates class or cozy dinner at Jean-Georges."

The Ness, Dong's trampoline studio in the nearby neighborhood of Tribeca, was also invitation-only when it first opened in 2019. Dong, a former professional dancer, hoped to cultivate an intimate community for the high-intensity, low-impact workout.

Corrie Aune for BI

But then the Ness got popular, and they relaxed this policy. Now, anyone can attend a drop-in class for $48. But extra amenities like the infrared sauna and cold plunge are reserved for members — who must apply and who are judged on the energy they bring to class and how they interact with other members and staff. There are currently just 35 openings — membership tiers range from $160 to $720 a month.

Even the biggest spender could be turned away for giving out the wrong vibes. Negative body image talk is an immediate strike against you. "If they come in the door and they're like, 'I just ate 10 cookies, I need to sweat. I need to get skinny in 10 days, I'm going to the beach.' That for us is always a no," she says. "We don't want any of that energy in our community."

"Fitness in New York can feel very transient," Dong explains. "There are so many studios and classes, and people often hop around." She likens the experience to dating. "Your first visit might be like grabbing coffee or taking a walk—not a steak dinner. That kind of deeper investment comes later, when there's a mutual commitment," she says.

"Our membership works the same way. It's reserved for people who are truly engaged with what we offer and who feel aligned with our community."

Corrie Aune for BI

Dogpound, a boutique Manhattan gym where Karlie Kloss, Taylor Swift, and Hugh Jackman have been known to work out, is already exclusive.

Until recently, Dogpound had planned to move to a referral-only model, says Xander Hodge, the gym's general manager.

Instead, Dogpound discontinued the most affordable — $708-a-month — membership, which covered just four personal training sessions a month. And they added a top membership tier that allows for unlimited sessions and costs $100,000 a year. The idea, says Hodge, is to preserve the feel of a committed, tight-knit community while ensuring the privacy of their A-list clientele.

On a recent afternoon, I was invited to try a group class. The all-black space was smaller than your standard commercial gym, sleek, but there were no frills — not even showers, though Hodge tells me they hope to add some as part of a planned expansion. After two sessions with the same trainer, clients are required to rotate to someone new, part of the gym's strategy to make sure everyone gets to know one another on a first-name basis.

There were just three of us — a mom of three who said she has worked out at Dogpound two times a week since 2020, and her friend, who occasionally tags along for a class. ("She is our reigning member," Hodge says of the mom after the class ended. "Anytime we have a charity event, she is the first one there bringing three friends!")

The workout was tough, a mix of dumbbell and bodyweight exercises and cardio. With so few of us, the individualized instruction was great. The class was also fun. I was surprised at how open my classmates were to socializing in between sets, chatting about weekend plans and bad dates. Two personal training sessions were happening nearby, and every instructor who passed our class introduced themselves with a friendly fist bump. One did a handstand.

It all felt remarkably warm and welcoming. Unlike the oversubscribed gyms and full-to-capacity SoulCycle classes I was used to, here I felt like I was working out among old friends. It was intimate and, yes, luxurious. As I left, I caught myself running the math to see if I could swing becoming a regular.

The next night, I joined Dogpound's Tuesday night run club on a running path along New York's Hudson River. The club is free and open to the public, but the seven other people who showed up were all current or former Dogpound members or staff. As we made our way past Battery Park, with a view out to the Statue of Liberty, half the group kept up a competitive pace — one was a serial ultramarathoner — while I hung back with the more talkative runners, keeping a more leisurely pace.

Corrie Aune for BI

I struck up a conversation with a fellow first-timer. She had joined Dogpound as a 30th birthday gift to herself and strength trains at the gym twice a week. Her enthusiasm echoed the feeling I'd had the night before: With fewer people around, it's easier to meet and bond with like-minded people.

It was a very different experience from Equinox, her previous gym. There, she says, she and her sister had split a single $325 membership card, passing it back and forth for months. The front desk, she said, never realized they weren't the same person.

Eve Upton-Clarkis a features writer covering culture and society.

Palantir is gaining ground with early-career talent — including some recruits who haven't even started college — thanks to cushy software engineering salaries and a growing appetite among younger techies for defense tech work. The company is also riding a tone shift in Silicon Valley, where working with the government is no longer taboo.

Palantir builds software that helps institutions — both government agencies and commercial companies — manage and analyze their data. In addition to building defense software for the US and allied militaries, the company also makes AI tools for health systems like Mount Sinai and HCA Healthcare.

The company appears to be hiring across the board, with open roles ranging from entry-level software engineers to government-focused business development staff, according to its job listings. While compensation information isn't publicized by most tech companies, including Palantir, public records from US work visa applications give some insight into pay for specific positions.

The data comes from filings from the first quarter of 2025 that companies submit to the US Department of Labor when hiring foreign workers on H-1B visas. Business Insider analyzed Palantir's filings to see where it's hiring — and what it's paying. The figures only refer to foreign hires and only account for base pay, not the bonuses and stock awards that employees receive.

Unlike tech giants such as Microsoft, Google, and Meta, which each filed thousands of H-1B applications during the same period, Palantir submitted far fewer. That may be in part due to the nature of its government work; some of these roles at Palantir could require US security clearance, according to Palantir job postings reviewed by BI. Security clearance can only typically be granted to American citizens, according to the State Department.

Palantir didn't immediately respond to a request for comment from BI.

Here's what Palantir is paying across key roles, from Forward Deployed Engineers to Machine Learning Researchers.

Deployment roles: Forward Deployed Engineers can make as much as $200,000 in base pay.

Forward Deployed Engineer: $143,000 to $200,000

Deployment Strategist: $120,000 to $160,000

Software Engineers can make up to $240,000 in base pay.

Steven Henry (left) and Jennifer Roth (Rright) of Goldman Sachs.

Goldman Sachs

Sales and trading divisions in Wall Street banks have been raking in record revenues.

BI spoke to a Goldman intern and partner about the training process.

Here's what it's like to intern for Goldman's sales and trading desk as the business hits new highs.

It's a good time to be a trader-in-training.

Whether you're learning about currencies, derivatives, stocks, or bonds — sometimes markets are, well, slow. Not this year.

From Trump's tariffs to the rise of AI, major shifts in how business gets done have fueled market volatility—and record revenues for banks—creating an ideal environment for aspiring traders to see fast-moving markets in action.

"We've been incredibly busy," said Goldman Sachs partner Jennifer Roth. "The markets have been volatile, so it's exciting to be on the trading floor," added Roth, the bank's global cohead of emerging markets and foreign exchange.

BI spoke with Roth and Steven Henry, a sales and trading division intern, to understand what one of the busiest years in trading looks like for college students working there this summer.

Henry, an MIT student, said he spent the first half of the summer in equities trading, and recently started on his second "rotation," as Goldman calls it, in mortgage trading.

Bank trading desks facilitate the buying and selling of financial assets for hedge funds, pension funds, and other institutional investors. They also help these clients manage risk using tools like options, futures, and other derivatives. The division at Goldman posted record revenues last quarter, up about 36% from last year.

The experience, Henry said, has been overwhelming — in a good way.

"I didn't expect to learn the amount that I have in such a short time. I think I can confidently say that during this internship so far, even just in the past few weeks, I've learned more than at any other point in my life."

Goldman Sachs' headquarters at 200 West Street in Lower Manhattan.

Momo Takahashi / Business Insider

The day-to-day of a busy summer

The interns on Roth's team help the sales and trading executives keep up with the news ahead of markets opening and synthesize what's in their flooded inboxes each morning. Interns also get to work on market research — analyzing what goes into a good trade decision.

"They also do pitches for us, so once a week they'll show what they've learned on the desk that week and pitch a trade to us, and we'll ask them questions so they can really illustrate their understanding," said Roth.

During his time on the equities trading team, Henry pitched stocks that he said weren't just theoretical exercises — but real ideas that business leaders could act on.

"We're researching real things that the desk would consider important to look at," he said.

The most exciting part of the day for Henry (and what he said he spends most of his time on) has been sitting next to traders — absorbing the fast-paced cadence of their work and asking questions.

"I usually try to spend most of my time sitting with traders and learning from them, trying to understand the language that they speak, what they consider important, how they go throughout their days," he said. "I think that's been the best way for me to actually learn about the products and see how it comes out in real life."

As for his schedule, Henry said he feels it's important to be ready to leap into action, before, during, and after the trading day.

"For me, we try to get in a little before the market opens," he said. "Then we stay with them throughout the day and see how things progress," he said, adding that as an intern, he is aiming for "a holistic view of the full day of a trader."

A seating area at 200 West Street

Emmalyse Brownstein

Getting a return offer on the trading floor

Roth started out as an intern herself at Goldman in 2002. Now, as a partner, she plays a key role in handing out offers to the interns she wants to work for her team after they graduate from college.

She doesn't expect interns to be financial experts, but she's looking for young people who eat, sleep, and breathe markets. After all, Wall Street traders are known to be at the desk for 10 or 12 hours a day.

"I want someone to express passion for the markets," she said, adding: "Ultimately, you want to really, truly love what you do."

She's also looking for people who have demonstrated an ability to learn quickly and jump into the action.

"There are so many smart young people out there. I want someone who I can sit next to who can be a team player," said Roth. "A lot of the training happens on the job, so I want someone who can pick up concepts quickly, who is willing to get their hands dirty and get involved in the nuances of each trade."

That means asking a lot of questions, but also showing you have grasped what you learned so far.

Interns should strive to illustrate "that they understand the answers when they ask questions," she said, adding:

"When I look back to when I was an intern, I wish I had asked more questions and took the opportunity to meet as many people as I could and learn as much as I could."

The author (not pictured) was diagnosed with ADHD at 32.

Delmaine Donson/Getty Images

I recently received an ADHD diagnosis at 32.

I've used coping mechanisms for years to make life easier without knowing why I was doing it.

Now, I'm learning about thriving with ADHD, and the confirmation of a diagnosis is validating.

Aristotle said that knowing yourself is the beginning of all wisdom. My latest 'ah-ha' moment is a long-suspected ADHD diagnosis, made official this month. According to the National Institute of Mental Health, themedian age for a mild ADHD diagnosisis 7. I'm 32.

I was hesitant to assign myself the label, since finding ADHD memes relatable is hardly a diagnosis, even when those memes feel like they were made with me in mind. Now that I've seen a specialist who confirmed my suspicions, the feeling of vindication is kind of exhilarating.

I've suspected I had ADHD for about 10 years

"When was the first time you suspected this?" the doctor asked.

Ten years ago, I was team-marking with other teachers, trapped for a full weekend with the task of grading hundreds of senior exams before the deadline. The other teachers were flying through essays, their red pens a blur.

I watched them for a bit, wondering how they were able to tune each other out. I graded two essays and then made some tea. I rewarded myself forfinishing another essaywith the slow removal of my jacket. Many buttons. Thrilling. And then one more essay, followed by a snack. The sound of my colleagues' pens was distracting. The sound of the kettle boiling, even more so. Speaking of which…more tea? A bathroom break? I was bored senseless.

"How many have you done, Tayla?" I'd tackled four in the time the others had each graded 12. I told myself it was because the other teachers were more experienced.

I developed coping mechanisms long ago to mask symptoms

I shared the news of my diagnosis with a friend from school. "Seriously? But…you're so productive?" she said, shocked. It was easy to slip through the cracks as a high achiever. ADHD diagnoses are often missed in girls — the ratio of boys togirls with ADHDis 3:1 in childhood, but in adulthood it's much closer to 1:1. Apparently, girls with ADHD are more likely to make an effort to mask symptoms.

I got straight As in school (bar physical science, which felt like torture) and graduated from university magna cum laude. Along the way, I'd unknowingly beendeveloping coping strategies, weaving them into my daily life. A major one was the subjects I chose.

In high school, I dropped two math classes in my final year; it wasn't my strong suit. In university, excelling in psychology and English was easy — I loved both majors and would happily fixate on them for hours.

I've had a daily to-do list for decades. I voice note myself constantly. My calendar is so detailed that it looks encyclopedic. I schedule meetings and my toughest tasks during my most productive hours. I lock my phone away during work because I'll scroll fruitlessly. And now I can see all of this for what it is: a plethora of coping mechanisms.

Even pursuing my writing career, I curated it around an ADHD diagnosis I didn't yet have. I struggle to write on topics I don't care about, so I built a roster of clients and publications in travel, a subject that obsesses me. Being self-employed has allowed me to tap into other interests, likecoaching peoplein writing personal essays. I've always gravitated toward the form. After a quick Google, it turns out many associate oversharing with ADHD, too. Hmm.

I'm throwing myself into learning. I'm reading books aboutthriving with ADHD. I'm following relevant accounts on social media, knowing that I now belong in these communities. The best time to get this diagnosis was probably 25 years ago. But I have it now. I'm not convinced this is the "beginning of wisdom" as Aristotle says, but it's the beginning of something. That's good enough for now.

The sun sets behind power transmission lines in Texas, on July 11, 2022.

Nick Wagner/Xinhua via Getty Images

For a large swath of the US, data centers are driving energy prices higher.

Wholesale electricity prices are up 22% from 2024.

Ratepayer advocates warn Big Tech's energy demand is hitting consumer wallets.

Your electric bills may have shot up in recent months, and you might be tempted to blame your roommate, who never turns the lights off, or your old window air conditioner unit.

It's not because of your roommate. It's not your window unit. It's actually Big Tech's fault.

Customers of the biggest regional power grid operator in the US could see their bills go up next year, largely due to skyrocketing demand for electricity coming from AI data centers.

Last week, PJM Interconnection closed its annual capacity auction with prices for wholesale electric capacity up 22% from 2024, another record-breaking year. As a result, monthly electric bills in PJM's territory, which covers 67 million customers, could increase up to 5% next year, the grid operator said.

PJM Interconnection territory spans thirteen states from the Midwest to the East Coast— including all or parts of Delaware, Indiana, Illinois, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, and Washington, D.C.

Every year, PJM's summer auction determines the cost of wholesale electricity for the following year. Though its territory doesn't cover the entire US, the energy industry looks at the PJM auction as a bellwether for electricity prices for the entire country.

PJM's territory includes Data Center Alley in Northern Virginia, home to the world's biggest concentration of data centers. It also includes areas of the country where data centers are rapidly expanding, such as Columbus, Ohio. The grid operator identified data center expansion as the primary driver of demand in its territory, which caused the jump in wholesale electricity prices.

After a decade of little to no growth, electricity demand in the US is expected to grow 2.5% annually through 2035, driven largely by data centers, according to the Bank of America Institute.

Utility bills are climbing faster than the pace of inflation, according to the US Energy Information Administration. That trend is expected to continue through the next year.

In Maryland, People's Counsel David Lapp has been urging state and federal regulators to intervene on behalf of residential utility customers and small businesses.

"We are witnessing a massive transfer of wealth from residential utility customers to large corporations—data centers and large utilities and their corporate parents, which profit from building additional energy infrastructure," said Lapp. "Utility regulation is failing to protect residential customers, contributing to an energy affordability crisis."

Got a tip for this reporter? Contact Ellen Thomas at ethomas@insider.com.

Two humanoid robots box during the 2025 World Artificial Intelligence Conference in Shanghai, China.

Ying Tang/NurPhoto

The World Artificial Intelligence Conference took place in Shanghai this weekend.

In a speech, Chinese Premier Li Qiang called for a global organization to coordinate AI safety.

US President Donald Trump, however, may be an obstacle to that.

At this weekend's World Artificial Intelligence Conference in Shanghai, boxing robots thrilled the crowd. But the real heavyweight bout is between the US and China over the future of AI.

The theme of the Shanghai conference, which was organized in part by the Chinese government and lasts until Monday, is "global solidarity in the AI era." In his keynote address, Chinese Premier Li Qiang called for a new global organization to coordinate responses to AI advancements.

"Overall, global AI governance is still fragmented. Countries have great differences, particularly in terms of areas such as regulatory concepts, institutional rules," he said, speaking in Chinese. "We should strengthen coordination to form a global AI governance framework that has broad consensus as soon as possible."

Li's pitch contrasted with comments made by US President Donald Trump earlier in the week. On Wednesday, the US president released his "AI Action Plan" and signed three executive orders. All of them, Trump said, were designed to free AI companies from regulatory burdens.

"From this day forward, it'll be a policy of the United States to do whatever it takes to lead the world in artificial intelligence," he said before signing his executive orders.

Trump's doctrine will likely benefit American AI companies. Many of them, like OpenAI, Meta, and Google DeepMind, submitted recommendations to the president and praised the new policies.

However, it's an open question whether forgoing stricter regulations in the United States will benefit humanity.

AI industry leaders have long warned about the threats AI could pose — everything from disinformation and economic inequality to total loss of all human control.

In 2023, a group of prominent AI scientists, including OpenAI CEO Sam Altman, Google DeepMind CEO Demis Hassabis, and Anthropic CEO Dario Amodei, signed a one-sentence statement calling for AI regulation.

"Mitigating the risk of extinction from AI should be a global priority alongside other societal-scale risks such as pandemics and nuclear war," it said.

Altman said last year that AI could have a "negative impact way beyond the realm of one country." He said the tech should be regulated by an "international agency looking at the most powerful systems and ensuring reasonable safety testing."

One way to do that is through an agreed-upon global framework similar to the Nuclear Nonproliferation Treaty, which is enforced by the United Nations and which all but four countries have signed. The UN tech chief, Doreen Bogdan-Martin, told the AFP on Saturday that the world urgently needed a global deal to regulate AI.

"We have the EU approach. We have the Chinese approach. Now we're seeing the US approach. I think what's needed is for those approaches to dialogue," she said.

The Trump administration, however, is likely to hinder any such international agreement. Beyond its own effort to loosen restrictions at home, it has largely dismissed other global collaborations in favor of its America First policy.

At the Shanghai conference, Geoffrey Hinton, a computer scientist known as the Godfather of AI, said international cooperation on AI would be difficult. He said few countries agree on basics like how misinformation should be policed.

He said there was one subject, however, on which the whole world seems aligned: Humans should not let AI supersede their control.

"So on that particular issue, it should be easy to get international collaboration," he said at the conference, adding, however, that it "may be difficult with the current US administration."

"But rational countries will collaborate on that," he said.

Etsy witches are selling spells for love, good fortune, and career success, priced from $4 to $400.

I paid a witch $18.65 for "extreme luck." It was surprisingly easy, but I had to wade through a lot of AI slop.

People may turn to the mystical more in times of heightened economic uncertainty.

I opted against the demonic misfortune curse.

Sure, my seatmate on a recent flight made the regrettable decision to eat a whole fried chicken, but she doesn't deserve supernatural torment. It also wasn't worth the $40 price tag.

I'm admittedly new to commissioning magic off of Etsy, a website I typically browse to pine after expensive home decor. I'm not big on ghosts, paranormal activity, or superstition.

I am, however, curious.

The Etsy witches are busy these days. Social media is peppered with people offering spells, testifying about their successful spiritual cleansings, and parodying mystic rituals. The US psychic services industry was worth over $2 billion last year, and that's projected to grow to $4.5 billion by 2033, largely due to online interest. If that projection is right, it's more than Americans spend on dog walking services today, but less than they spend on nail salons. While the recent success of digital hexes could be a sign that people are bored and leaning into internet trends, it also hints at something more serious.

"Magic is among the things that people turn to when things are becoming uncontrollable, when things are becoming uncertain, when you know the normal methods you use to shore up your life and provide some certainty don't seem to be working anymore," Michael Bailey, a history professor at Iowa State University who specializes in medieval Europe and witchcraft, told me.

I can empathize with that. I, too, have a lot of worries about my future and the world. So I spent $18.65 (plus tax) on a spell to bring me extreme luck. I'm not feeling especially unlucky right now — I have many people that I love, and my boss lets me write things like this during work hours. But it seemed like a reasonable price for some extra good fortune, and I would really like a New York City apartment with laundry in the building.

Etsy witches work their magic on your career or love life for prices ranging from $4 to $400

Jamie Mejia, 31, lives in Miami and swears by her Etsy witch results.

About a month ago, she enlisted one for a reading about her love life, which cost her about $5 for each question she asked. Mejia had sensed that her partner wasn't ready to commit to a serious relationship, a feeling the witch validated. She said it brought her the closure she needed to end things. When she returned for a second reading, Mejia received good news: 2026 will be a big year for her career and personal life.

For prices that range from $4 to $400, the Etsy witches offer anything I might need. I could increase my chances for long-lasting beauty, a dream job, money, protection, warm weather, a perfect wedding, or a loyal sugar daddy. I could inspire an ex to call me or motivate a crush to ask me on a date. Curses were also on the table, including promises of "revenge, pain, and suffering" for my enemies, along with the aforementioned demonic misfortune.

Most of the spells, including mine, had extra-long wait times due to a "high volume of requests." I chose to ignore the flood of AI-generated images of the alleged witches: several silvery-haired wrinkled women that didn't look quite human, videos of a sage cleansing ritual where the hand had extra fingers, and perfectly-arranged altars that were too good to be true. It seemed weird that many of the spells were on sale — is it possible to find your soulmate at a discount? For the purposes of this story, it was important that I trust the process.

It's worth noting that magic has been banned on Etsy since the mid-2010s. Most of the sellers have disclaimers that their work is for entertainment purposes only. A representative for Etsy didn't respond to my request for comment. Based on the thousands of positive reviews and plentiful social media testimonials, however, there are true believers among the internet-magic curious.

"Part of me obviously has lost faith when it comes to relationships, so knowing that it gave me a little bit of hope," Mejia said, adding, "I don't think it's fake, I think it's real."

My witch sent me photo proof of my good luck spell.

Etsy

Turning to the mystical when other avenues to success seem blocked

Meija told me that she's turning to witches to manifest companionship and job security in a tough market for both. Assuming most of the Etsy reviews are written by real people, she isn't alone. Many of the sellers have thousands of reviews and average between 4.5 and 5 stars. Some happy customers said spells helped them pass an exam, land a new role, dismiss a traffic ticket, have a sunny bachelorette weekend, or feel a little bit less stressed. Most said they are still eagerly awaiting their results.

In the most recently available 2017 Pew survey of American adults, 41% of respondents said they believed in psychics, 42% said they thought spiritual energy could be located in physical things, and 29% said they believed in astrology. A 2019 IPSOS survey also found that nearly half of respondents said they believed in ghosts. My colleague Emily Stewart wrote about this last summer: It isn't new that people are willing to shell out money on magic.

But the latest success of Etsy witches may be a sign of the times. Americans of all ages have told Business Insider in recent months that they're frustrated by long job searches, feeling nervous about finances, or holding off on big life decisions like having babies and starting a business because the economy feels unpredictable. Consumer sentiment markers dipped in July, and employees are less confident in their companies lately. Another Pew survey conducted last September found that 16% of adults feel lonely all or most of the time, with higher rates among Gen Z and millennials. Bailey said he isn't surprised that people are keen for an extra chance at financial stability, love, and relationships right now.

"When you're feeling particularly uncertain, you're more inclined to the 'try anything' approach," he said, adding that magic has long been a way people try to "swing the odds in their favor."

Thirty-six hours after I submitted my order, my witch sent me photo proof that my spell had been cast: an altar with a brightly-lit green candle, some crystals, and a couple of tarot cards. Over DM on the Etsy website, she told me I have "powerful support from the Universe," and the "The Luck Alignment Ritual" has been activated, "so it is done, Amen."

All she needed from me was my birthday, two sentences about my intention, and a working credit card. We never talked, and I don't know what she looks like. That seems to be the case for most witches: you can order luck off the internet with a transaction that looks a lot like buying a Shein haul or bowl of DoorDashed pad thai.

The whole thing felt spooky, and I'm not convinced Etsy magic is the healthiest way to cope with anxiety. But if I find an affordable apartment with laundry, I might be willing to credit divine intervention.

Denise Segled during the Koningsdag celebration in the Netherlands.

Courtesy of Denise Segler

Denise Segler was laid off from her role as a project manager at Amazon in 2023.

Seeking a fresh start, she moved to the Netherlands in 2024 for a calmer and more affordable life.

Segler told BI that she's saving money, feels more relaxed, and her small business is thriving.

This as-told-to essay is based on a conversation with Denise Segler, 54, who moved from Seattle to Haarlem, a city in North Holland, the Netherlands, in 2024. The conversation has been edited for length and clarity.

I fell in love with Europe at 18 during a school trip and promised to live abroad someday. I didn't know when or where, but I would make it happen.

After that, I asked myself: What do I want to do with my life? I also questioned what was keeping me in the US.

A lot of different things were pulling me toward Europe. I wanted to be my own boss and work as a freelancer. But health insurance in the US is incredibly expensive, and that's not the case in much of Europe. I also think Europeans have a better quality of life and work-life balance. In addition, the political climate in the US added a sense of urgency.

Europe was calling my name

When 2024 came around, I knew it was finally a good time to take a chance abroad.

I had earned higher-level project management credentials and started actively promoting my own business as an IT project manager.

I had also taken a trip to Ireland. I spent three weeks there — two on my own, and then my 27-year-old joined me for the last week. During that trip, I realized: OK, I can do this. I can go somewhere unfamiliar and be just fine.

A street in Haarlem, Netherlands.

tunart/Getty Images

I researched different European visas and discovered the Dutch American Friendship Treaty (DAFT) visa. It allows Americans to live in the Netherlands as independent business owners. They just need to maintain a minimum of €4,500 ($5,278) in a business bank account.

The visa was attractive to me. I also found out that the Netherlands had more affordable health insurance. Then I looked around, and other things were cheaper: cellphone and internet services. I thought, "Why not give that a try?"

While you can do it yourself, I used a Dutch legal professional to file my visa paperwork. The legal office submitted my visa application and documents to the Dutch government on my behalf in August 2024 and let me know the visa was approved in September. I landed in Amsterdam on November 5.

The Netherlands is the perfect place for me

Before I moved to the Netherlands, I had never visited. But I received a lot of advice from people who had. Everyone had wonderful things to say — it was beautiful, and the people were fantastic.

I live just south of Haarlem, the capital of North Holland, in a really cute neighborhood with shops, restaurants, and cafés. I feel very lucky, there's a train station just an eight-minute walk away from my apartment, and I'm right near a shopping area with all kinds of grocery stores.

In some ways, the area reminds me of parts of Seattle, like the South Lake Union neighborhood.

A city street in the town of Heemstede, in the province of North Holland, during the Koningsdag celebration.

Courtesy of Denise Segler

Before moving to the area, I hired a makelaar, a real estate agent, who helped me find a place to live. There's a housing shortage in the Netherlands, so you have to be either very flexible about where you live or be prepared to spend a lot of money.

I was very lucky and ended up getting the first apartment I looked at. I had to pay six months' rent in advance because, as someone new to the country, I didn't have any local rental history.

My apartment has a bedroom, a bathroom, and a small second room that I use as an office. There's also a combined living and dining area that leads past the kitchen.

I spend more on housing but less on everything else

I am paying more for housing in the Netherlands, about €1,735 ($2,041) for my apartment, but all my other bills are significantly cheaper than in the US.

I pay €38 ($45) a month for internet and TV, whereas in the US, I paid over $100. My health insurance is also much cheaper here.

Legally, you must have health insurance in the Netherlands, and there are a variety of insurance companies to choose from. In the US, I was on COBRA, which cost over $800 a month. Here, I pay €190 ($224) a month. It could be cheaper, but I added dental coverage and extra benefits for chiropractic care.

Since I've been here, I've had my teeth cleaned once by a dentist, and that was about €150 ($176). The insurance paid half, and I paid the other half.

A windmill in Heemstede, a town in North Holland.

Courtesy Denise Segler

I worried that food would be more expensive in the Netherlands, but it's not that bad. Produce is pretty cheap. For example, eggs usually come in packs of 10, costing between $3 and $4, depending on the type.

The produce here is fantastic. There are farmers markets all over. I go to one every Wednesday, and I have to be careful because I always come back with all kinds of potatoes and cheeses. I think the bread is better here, too; many stores have in-house bakeries.

There are pros and cons to living here

English isn't an official language of the Netherlands, though most people speak it fluently.

French is also commonly spoken, which works well for me. While I wasn't fully immersed in French, I practiced it five days a week for over a decade, starting when I was about nine years old.

The locals are generally welcoming. I have seen someone shouting at people speaking a language other than Dutch or English, but only once or twice in the several months that I've been here. No one has been angry with me for speaking English. I think they take me as a tourist and are glad that I have a few words of Dutch.

A canal between Haarlem (left) and Heemstede (right).

Courtesy of Denise Segler

The people here are kind of direct, but I don't mind that much. Once, I went to get my hair cut, and the hairdresser commented, "Oh, you have to color your gray." I said, "No, I like my gray."'

It can be hard to make friends, but there are meetup groups and Tinder, if you want to date. I do miss my chosen friends and family, and I have standing phone calls with them every Sunday night.

Moving to the Netherlands was the right decision for me

My life is more relaxed in the Netherlands because, honestly, I feel safer here.

There aren't nearly as many guns, and I'm living in a safer neighborhood than I was in the US. I'm also not worried that a medical emergency is going to bankrupt me.

I'm paying significantly less in bills, and the money I am saving every month on health insurance is going toward my savings and my business.

My business is also about ready to take off. I joined two networking organizations of business owners, one based in the Netherlands and one based in the UK. I am working with a business coach, and I will be hiring a branding expert next month.

Haarlem

scanrail/Getty Images/iStockphoto

My visa expires in July next year. I can request an extension, which I believe would grant me an additional three years. At that point, I would have been here five years, and I can apply for permanent residency, or, after taking Dutch classes, citizenship.

I don't know if I want to become a citizen of the Netherlands, but for now, I'm just happy to be here because I can support myself.

Lydia Hinds, 81, says a part-time job at Home Depot is her only option to keep her and her husband, 90, financially afloat.

Michael J. Fiedler for BI

Noah Sheidlower spent two days following Lydia and Bill Hinds, a married couple of nearly 30 years, who say they're just scraping by in central Connecticut. He reviewed their financial records for this story. He also interviewed more than 90 workers in their 80s and 90s, and 30 researchers and nonprofit leaders focused on older Americans at work. This story is part of a series on people working past 80.

Lydia Hinds, 81, collapses onto her red couch, takes a deep breath, and lets out a defeated yell.

She just returned home from what was supposed to be a five-hour shift wiping down appliances and helping customers at a Home Depot in Berlin, Connecticut. In the first four hours, she paused several times to catch her breath, so she clocked out an hour early.

"I feel trapped working, but I can't stop working," Lydia says, sitting up to cuddle her basset hound, Brigette. Her husband, Bill, gives her a kiss but lets her be. The 90-year-old would like to get a job to help Lydia pay the bills, but because of health problems, there's little he can do.

"I feel so guilty that I can't work," Bill says.

"You can't work because of your age and your health issues," Lydia snaps back. "There's no sense feeling guilty about it."

Lydia snuggles with her basset hound, Brigette, who comforts her anxieties over money.

Michael J. Fiedler for BI

A certificate for a regional award that Lydia received from Home Depot, praising her dedication to the job, sits on their coffee table. Since starting in 2022, she's received two promotions, despite being unable to climb ladders or lift heavy objects because of her heart failure diagnosis last year. In a photo attached to the award, she's smiling from ear to ear. Now, the best Lydia can muster is a muted grin.

If she stopped working and lost her $300 weekly pay after taxes, she and Bill fear they couldn't afford rent. A few weeks back, they had 44 cents in savings. They weren't sure what they would eat for dinner.

Three printed-out job applications for remote customer service positions lie near her award. She doubts she'll get further than one interview, but each application is a glimmer of hope. "What company would hire an 81-year-old?" Lydia asks. "Hopefully one of them."

A better-paying, less intense job could give them the boost they've yearned for, especially as Lydia's weekly hours some weeks have been cut from 22 to 17.

Lydia is one of over half a million Americans over the age of 80 who still work as managers, retail salespeople, lawyers, drivers, and other jobs — over 4% of the Silent Generation. That number has gone up to 4.2% from 3.6% in the last decade due to various factors making full retirement impossible or undesirable for a growing number of seniors, according to a Business Insider analysis of Census data.

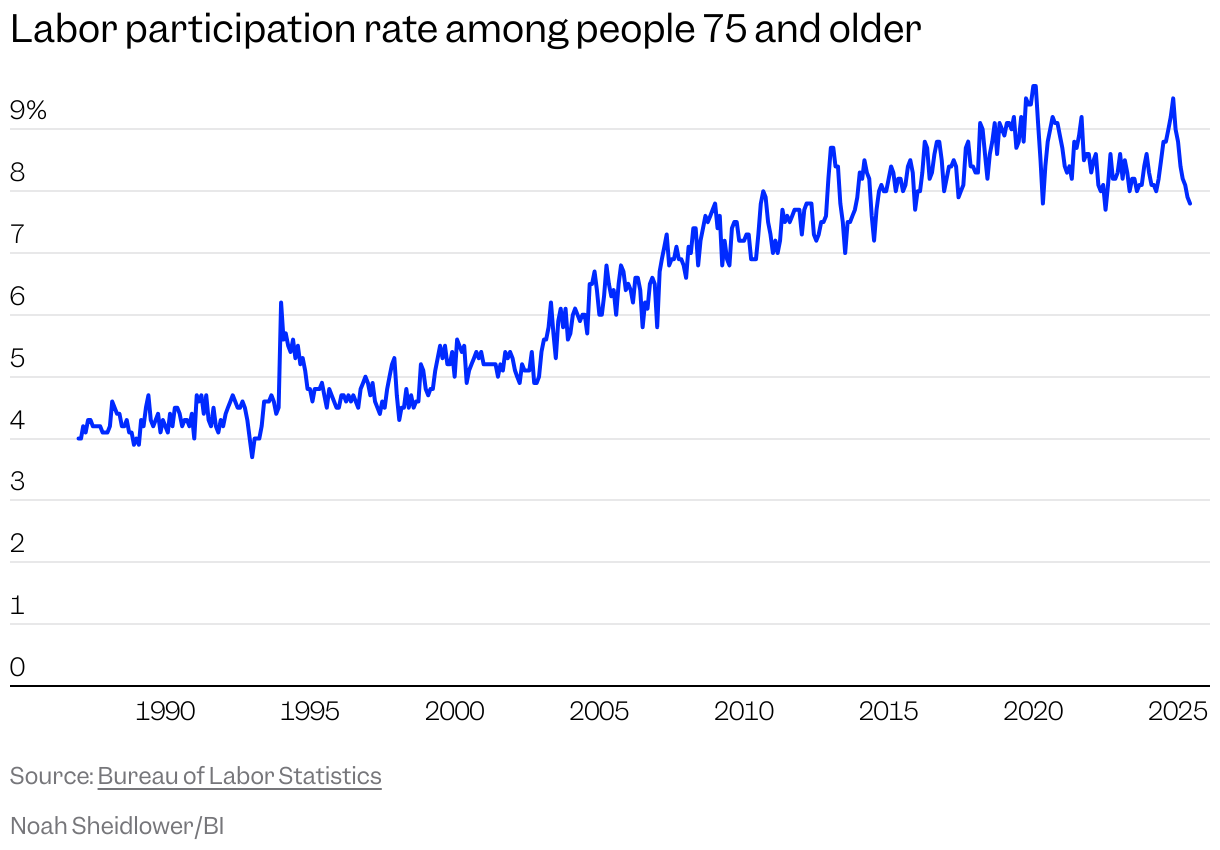

"We do know that the 75-plus demographic is the fastest growing segment of the workforce," says Carly Roszkowski, vice president of financial resilience at AARP. Americans age 75 and over are twice as likely to be in the workforce now as they were in the early 1990s, according to Bureau of Labor Statistics data.

Those in their 80s or older are part of the Silent Generation of Americans born between 1928 to 1945. They grew up against the economic backdrop of the Great Depression and World War II, and learned to be financially cautious after seeing what their parents endured. However, they didn't have access to the same kind of personal finance advice and tools that are prevalent today.

Lydia and Bill Hinds are worried that if her income goes away, they won't have many options to keep their home.

Michael J. Fiedler for BI

In recent months, more than 90 workers aged 80 and older told Business Insider in interviews how health challenges, loneliness, and increased cost of living all play into their decision to work at their age. Over a dozen say all they could find were minimum-wage jobs, and many work despite medical diagnoses. The financial strain bleeds into their relationships with spouses and children, and exacerbates a pervasive feeling of isolation.

Right now, the Hindses take in $4,600 a month from their Social Security, Bill's pension from a TV station in Connecticut, and Lydia's monthly wages. Monthly rent for their one-bedroom apartment in a 55-plus development is $1,400, their car payment is $625 a month, their car insurance is $236 a month, and their Medicare combined is $426 a month. On top of that, they have emergency medical expenses, medications, grocery and gas bills, and utilities. They're left with close to nothing at the end of the month.

"I keep thinking, 'What happened that we can't go out?'" Lydia says of the couple's social life. "But the rent's gone up, and it's eaten up most of the Social Security money. We're in deep trouble."

Healthy enough to work into their 80s

Bill and Lydia say their financial mistakes were ones anyone could make. They never gambled, their investments weren't too risky, and they worked in decently paid jobs their entire careers.

Still, some miscalculations, unavoidable health issues, and poor timing have put them in a wobbly financial situation.

"Every month when it's time for my Social Security check, I get really tense. I'm so afraid it's not going to come," Lydia says. "If we don't get that, we're out of here. We're on the street."

Lydia says she tried to stay positive even though her financial situation worries her.

Michael J. Fiedler for BI

The number of cost-burdened households — those that spend more than 30% of their income on housing expenses — age 65 and older has steadily risen since the early 2000s. Research from the Joint Center for Housing Studies at Harvard University found that among adults age 75 and older who live alone in metro areas, only 13% could pay for assisted living without having to dig into their assets.

"I wish I had saved just $20 a week in my retirement account all those years ago," Lydia whispered during her shift. Even a small nest egg would relieve her stress. She has under $1,000 left in her 401(k) from Home Depot, down from nearly $10,000 at its peak, as she pulled out money twice for medical and day-to-day costs.

In 2022, Bill and Lydia needed additional income. During the pandemic, they'd both suffered from health issues, including Bill breaking his leg, which kept them from working. They relied solely on Social Security, Bill's small pension of $335 a month from his time at the local TV station in advertising sales, and some savings. But when they couldn't sustain their lifestyle anymore that year, Lydia drove down the road to the closest Home Depot and applied for a job. Home Depot hired her at $16 an hour in the electrical department. She was 79.

Lydia works between 17 and 24 hours a week, though her hours some weeks have been cut.

Michael J. Fiedler for BI

"I loved it at first, and I still enjoy my customers," Lydia says. "But when I started there, I didn't know I had heart failure."

When Lydia noticed tasks like sewing curtains and gardening knocked her out, a doctor found that her heart was not pumping nearly enough blood. At work each day, she's expected to clean appliances, keep aisles tidy, and help customers with their needs for $19.55 an hour. Still, she kept her sense of humor.

"When I got the echocardiogram, I joked with the doctors and told them, 'I forgot to tell you I'm pregnant,'" Lydia says. "They got a big laugh out of that."

As her condition worsened, she would have to catch her breath just from walking down an aisle. Conversations with customers and coworkers, who call her "Ms. Lydia," keep her ignited.

She says she's thankful that Home Depot has given her time off with pay, as part of her sick leave benefits, to go to doctors' appointments. She used Connecticut's paid family medical leave for six weeks because of her heart failure diagnosis.

Home Depot didn't respond to a request for comment for this story.

Lydia isn't alone in her battle between work and health. Similar circumstances have pushed many of those who are healthy enough to continue working. Others in her position may need the income, but aren't physically able to work. Beth Truesdale, a research fellow at the W.E. Upjohn Institute for Employment Research, says a "shocking number of people" are pushed out of the labor force in their 50s and 60s, let alone their 70s and 80s.

The cost of medications and medical procedures has eaten into the Hinds' savings.

Michael J. Fiedler for BI

The percentage of people who are working drops sharply starting around age 51, across all genders and education levels. Truesdale's calculations from 2020 showed a roughly 20-point fall in the percentage of people working at age 61 compared to 51. That's not mainly because of early retirements, she says. It's because of factors like poor health, caregiving responsibilities, and physically demanding roles.

Dozens of older Americans told BI over the last year that they had no choice but to retire earlier after a diagnosis or injury. Many rely solely on Social Security, which is about $2,000 monthly on average.

Lydia's coworker, Tony Sparveri, 80, works for a similar reason as her. He started part-time at Home Depot two decades ago in the gardening department before transitioning to a full-time kitchen and bath design consultant. He's not on his feet all day, and says the work makes him feel youthful. He earns more than Lydia and works mostly for financial reasons, as taxes on his home and rising costs have burdened him and his wife.

Tony Sparveri, 80, says he works at the local Home Depot to give himself and his wife a money buffer.

Michael J. Fiedler for BI

"Mentally and physically, I feel really good, and that's a blessing," Sparveri says. Still, he's concerned that many older people will continue to be hurt by rising prices and economic uncertainty. "People are suffering, and I don't want to put myself in that position."

Love keeps them going through financial ups and downs

One afternoon, Lydia searches every nook and cranny of the apartment in search of a CD by Bill's former jazz ensemble, recorded in 1996 with jazz pianist Bill Mays.

"It's blue and yellow. I've looked everywhere," Lydia calls out to Bill. "There's no way I lost it!"

He walks to a cabinet and pulls it out. She puts it into the CD player and starts dancing, humming the melody to the first track. Bill looks on with a slight smile. He started playing piano when he was 3, performed with a swing jazz band, and hosted an FM jazz radio show in Austin.

"Most of those people are dead," Bill says of his old bandmates.

"Well, you're not," Lydia quips.

Bill and Lydia have lived in their current apartment for six of their nearly 30 years of marriage. This is Bill's second and Lydia's third marriage, and each has children from previous spouses. Lydia lost much of her savings in her 40s when her second husband abruptly closed one of the successful office and mail service stores they started together. He declared bankruptcy very shortly after.

Lydia says she tries to stay active, despite her diagnosis of heart failure.

Michael J. Fiedler for BI

"It all went down the tubes," she recalls, noting she was able to get a previous job back shortly after. "I still don't know how I got through that."

They didn't know each other at the time, but while Lydia was recovering from that financial setback, Bill was making $90,000 a year from performances and his work at the TV station. Lydia met Bill through a dating service in 1995. He picked her up for their first date in a white limousine, wearing a camel-hair coat.

"I was going on dates with three women at the time, but when I saw her, I dropped them all," Bill says.

"He had glasses three times bigger than he needed, which I took care of," Lydia jokes.

Like any marriage, theirs has had its ups and downs. After a brief stint in Florida, they returned to Connecticut and spent most of their savings on a house that required more repairs than they had expected. Lydia had moved on from the now-closed mail stores and was working as a real estate agent, but says she rarely made enough money to be comfortable. Bill had left the TV station in 1994 to focus on his band and was playing at weddings, teaching piano lessons, and selling pianos. They had been able to save a little throughout their career, but never enough to think they could retire.

"We put almost all of our money into that house," Lydia says. She says they bought it for $185,000 in 2002 and spent more than $100,000 on renovations. "It looked a lot better, and we figured we'd flip it and do OK."

Then the 2008 recession hit "like a ton of bricks," Bill says.

At the time, they had $75,000 invested in the market, but as the market fell, they pulled from their account to pay for their increased mortgage and property taxes. The couple hoped they'd get some money out of the home they'd renovated. But they defaulted on their mortgage in 2015, and a forced sale brought only $115,000. They filed for bankruptcy. The income from a side business Lydia had started to help people downsize their homes, and the piano lessons that Bill gave, weren't enough.

They were among the more than 10 million Americans who lost their homes due to the Great Recession. The S&P 500 took over five years to fully bounce back after dropping more than half its value from its high in 2007 to its lowest point in 2009. For thousands of households approaching retirement age, this meant working longer after their savings shriveled.

"I take a lot of responsibility. We've made mistakes, but also, who knew a recession was coming?" Bill says.

"We all make mistakes, honey," Lydia says.

Lydia and Bill say they get by each day thanks to having one another.

Michael J. Fiedler for BI

While Americans on average are saving close to the recommended 15% of their income for retirement, many in their 80s and 90s grew up before financial education and 401(k)s were prevalent. Not saving enough was a common regret among the over 3,800 older Americans who shared with BI their retirement regrets and what aspects of their lives they would redo if they had the chance.

Maura Porcelli, a senior director at the National Council on Aging, says the organization "saw people who thought they had done their due diligence in planning for retirement, the sort who thought their monthly budgets were going to be sufficient, who had all those hopes dashed."

"We know that a good number of older adults are susceptible to a major life event that can knock out a major chunk of their savings," she says.

According to the Federal Reserve's Survey of Consumer Finances, the bottom fifth of households headed by someone 75 and older had a net worth of about $75,000 in 2022, including equity built up in their homes.

For now, the Hindses are bracing for another life-shattering event.

"If I lose her, I don't know what I'm going to do," Bill says. "She feels the same way."

Working to survive and holding on to each other

Some days after work, Lydia sits at her computer and applies for any job she could reasonably do. She tries to appear as sprightly as possible in her applications, sometimes emphasizing how she graduated from the University of Hartford mid-career in 1994. Though she omits her age from her résumé, she suspects that employers have been able to tell, preventing her from landing anything higher-paying than Home Depot.

To counter her many rejections, she started building an online business selling funny gift cards, bags, and clothes. She hired a company to design her website, which cost a few hundred dollars. She works with a print-on-demand company to secure merchandise. She hopes it will take off enough that she can work fewer hours at Home Depot.

When it comes time to pay the bills, Lydia says she hopes they have enough left over for groceries.

Michael J. Fiedler for BI

There is little concrete data about the prevalence of potential ageism among workers in their 80s. Companies are prohibited from age discrimination against workers 40 and older per the Age Discrimination in Employment Act. Many of the dozens of workers BI spoke with say they suspected their age hindered their progress at work or hurt their job applications.

"Managers are already thinking that 60 is too old, so there's little hope for someone who is much older," says Janine Vanderburg, who founded the anti-ageism nonprofit Changing the Narrative. "Many of the job boards for older workers are focused on lower-paid jobs where there's a demand. If you cannot pay your mortgage, your rent, whatever it is, and you need to work, it's better to do something than nothing."

Though programs like the Senior Community Service Employment Program help lower-income Americans 55 and older get job training, the two dozen aging and work researchers and organization executives BI spoke to agreed there should be more resources for older Americans in the workplace. This could include more conversations with workplace leadership about advocating for older workers, more training on technology topics like AI, or local legislation codifying more protections against ageism.

Lydia and Bill hope to move out of their apartment before their rent rises again. It's increased by nearly $300 a month since they moved in 2019, but they have nowhere to go. They're waiting for an open cottage at a nearby care facility, which would cost $1,650 for a one-bedroom unit, but they've rethought whether that would be feasible financially.

"I want to be in a place where if something happens, we're still together — or at least we can visit each other easily," Lydia says. With all the financial strain, some days, Lydia wants to give up and say, "The hell with it."

Bill can no longer work, but he spends as much time as he can with Lydia.

Michael J. Fiedler for BI

The couple attributes their longevity to their connection. They say they rarely fight, and when they do, it ends with laughs and comfort.

"We're soulmates," Lydia remarks, pointing to Bill.

Their relationship is vital because many people in their community, she says, are not well enough to live active lives. Plus, Lydia no longer speaks to her daughter after years of a souring relationship. Bill's relationship with his children is tighter. For his 90th birthday, most of his family flew to Connecticut. They're about to become great-grandparents.

It's hard to maintain friends on a budget, Bill says. They've set aside some money to visit a friend on Cape Cod in October, and Bill has plans to see a film with a friend. One of the downsides of aging, he says, is losing friends left and right. Many have died, while others have drifted away. Their Christmas dinner table of 10 a few years ago has dwindled to just three.

Amid financial frustrations and loneliness, they find moments of solace. Now and then, they drive the half hour to Hartford in their 2023 Hyundai Elantra for a concert or to the shore with their dog.

But often, it's the little moments that distract them from their financial anxiety. For the first time in five years, Bill sits at the piano in their community's clubhouse. He strikes a few chords, cringing as the notes sound slightly too dissonant for his liking.

"I have perfect pitch," Bill says.

"When I shout, he can tell me what note it is," Lydia whips back.

From memory, he plays selections from Claude Debussy's "Clair de Lune" and Frédéric Chopin's "Nocturnes," missing a note here and there to his frustration. Tears stream down Lydia's face as he serenades her with the out-of-tune piano. When he finishes a prelude, she hugs him tightly.

Bill's mind is still sharp, despite not teaching for years. He recently serenaded Lydia on the piano.

Michael J. Fiedler for BI

It's moments like these that keep her going, she says, holding his hand on the walk back home. Once there, Lydia takes a green binder and places it on her coffee table. In it are 30 pages of notes in preparation for a September trip to New York City for Bill's 91st birthday.

A dozen pages are devoted to receipts, directions, and other logistics, like a fancy Italian dinner at Carmine's and a $550-a-night hotel room on Broadway. But given their finances, they've canceled the dinner and are just doing a day trip without a hotel stay. They want to save for Lydia's birthday in August.

"I wanted to do something special, but we can't swing it," Lydia says, grabbing a tissue to wipe her eye. "A lot of people don't make it to 91."

One page sticks out. It's a receipt for the Broadway musical "Buena Vista Social Club": Two front-row balcony tickets cost her $700. She's paying $50 a month through November via a buy now, pay later app. Bill has long loved the music, and though the tickets were out of their budget, she says it's worth it. For just a day, they will feel wealthy.

Nothing, not even the medical bills protruding from her desk, her dwindling paystubs, or a dozenth new medication, would get in the way of that.

Ann Francis thought grad school would be her ticket to a stable and fulfilling career. Nearly two years later, she's hoping a pivot to nursing will get her out of a deep financial hole.

Since earning an MBA in 2023, Francis has struggled to land human resources roles. She said she's received some government assistance to help cover food and rent, but that it hasn't been enough, and she's now at risk of eviction. Earlier this year, despite carrying around $50,000 in student debt, she decided to pursue training for a new career.

In June, Francis completed a six-week, 90-hour nurse training program. After passing the state exam, she earned her certified nursing assistant license — a credential she hopes will finally open doors.

"I'm basically starting over — that's the part that bothers me," said Francis, who's in her 50s and based in the Northeast US. "But I have to do what I have to do to survive."

Francis's experience reflects a broader shift happening in the US labor market, where workers sidelined by slowdowns in white-collar hiring are considering pivots to more in-demand sectors. Amid economic uncertainty, ranging from tariffs to the early impacts of AI adoption, US businesses are hiring at nearly the slowest pace in over a decade. In addition, MBA degrees aren't paying off like they used to. Still, a few sectors, including healthcare, have continued to hire at robust levels.

"I'm very confident the jobs are there," she said.

From February to May, private education and health services saw the strongest job growth of any sector. In healthcare, jobs are especially plentiful at hospitals and in individual and family services. In June, only state and local government education added more jobs, while many sectors like professional and business services and financial activities shed roles.

"If you're not a teacher, if you're not a nurse, and you're not a doctor, you're not seeing those opportunities," Cory Stahle, an economist at the Indeed Hiring Lab, said of the June jobs report.

Finding a career that aligns with work experience and offers more job opportunities

In 2016, Francis immigrated to the US from Jamaica, sponsored by her then-husband. She received her green card the following year and began working part-time as an informal caregiver for older adults while she waited for formal work documentation.

By 2018, she'd secured her work authorization and was working at a day care that she said paid around $11 an hour. Over the next few years, she worked a wide range of gigs, including as a Lyft driver, a contact tracer, and a customer service representative, but none offered the financial stability she was looking for.

In 2021, Francis enrolled in an online master's program at the for-profit school DeVry University, hoping it would improve her chances of landing a job. By October 2023, she'd earned an MBA and a graduate certificate in human resources management — and was actively applying for HR jobs while continuing her part-time caregiving work.

She hoped her graduate studies would help her leverage the professional experience she gained before moving to the US. Francis said she earned a bachelor's degree at an overseas university and spent two decades working at a vocational training organization in Jamaica. In her final role, she managed student services, overseeing everything from student intake to graduation.

"In my heart, I'm thinking this will allow me to transition to the next level," she said.

But over the next year, her job search led nowhere. She reached out to an HR professional for advice, and the response was discouraging. They said her recent work experience didn't align with the roles she was pursuing, and that this was likely working against her.

In addition, former President Biden's Education Department in January announced debt cancellation for 4,100 borrowers who were found to have been defrauded by DeVry for misleading prospective students about their job prospects. The charges spanned 2008 to 2015, years before Francis attended the program, and she said that she was happy with her experience there.

"I have no regrets about attending the institution," she said. "It was a good program with great professors, and I gained knowledge while there."

Still, after two years of job hunting, Francis started thinking it was time to change course. She reflected on her recent work experience — caregiving — and began looking into nursing programs. She ultimately decided on a six-week certified nursing assistant program she said cost about $1,900.

Francis saw nursing as a practical path forward because she sensed there was a high demand for workers in the industry. A nurse she knew told her she'd "never been out of work," and Francis said there seemed to be plenty of postings on job platforms.

"When I went on Indeed, I saw many, many jobs," she said.

Looking ahead, Francis said she's optimistic she'll be able to land a nursing role — and that she recently interviewed for a position at a long-term care facility. She said she's also signed up for freelance nursing apps like Clipboard Health and Shiftmed.

Over time, she'd like to explore healthcare training or administrative positions — roles she feels would better draw on her past experience and education. But in the meantime, her unstable financial situation continues to weigh heavily on her.

"The uncertainty of how long this joblessness will continue is extremely stressful," she said. "But I believe that once given an opportunity, I will rise above my current situation."