Tuesday, 31 March 2026

Monday, 30 March 2026

I used AI to dispute a $1,200 dental bill. I don't see the glory in wasting my energy on tedious life tasks.

Courtesy of Jamie Phillis

- Jamie Phillis faced a surprise $1,200 dental bill after visiting a new dentist closer to home.

- AI tools like ChatGPT helped her identify billing issues and submit an appeal to her insurance.

- Her appeal was denied, but she never had to pay the bill.

I've always enjoyed good dental health, having just one cavity in my 33 years. Some of this I attribute to having the same dentist since I was 4.

Throughout my adulthood, my dental office felt like the only medical environment where I never had to worry about coverage through my ever-changing insurance providers or getting a massive bill in the mail.

That changed when my well-meaning husband recently suggested I find a dental office closer to our new house. It made sense to forgo a 45-minute commute to my appointments, and I was intrigued by the promises of more modern practices equipped with sleek offices and luxuries like ceiling-mounted TVs.

It was a pleasant experience until I was hit with a massive bill I didn't expect. I turned to AI for help fighting it.

After my first appointment at a new office, I was presented with a $3,320.49 bill

I'd only gone in for a cleaning. To the provider's benefit, I'm an easy upsell, especially for anything health-related. When they recommended an at-home treatment for gum disease, a retainer for my teeth grinding, and a 'full mouth irrigation' for gum health, I agreed, despite them not being covered by insurance and requiring high out-of-pocket costs.

It added up quickly, and before leaving the office, I regretfully paid the $2,111.29 I owed for the items not covered by insurance, which included tax and a credit card fee. I wished I had waited before agreeing to the extra services and done more research before moving forward; however, I naively had no concerns about the remaining balance that would be sent to my insurance company.

A few weeks later, I was floored when my dental insurance informed me that my responsibility was $1,201.80

The primary issue was that, despite finding the dental office on my insurance site, I was paired with the only doctor at the practice who didn't accept my insurance — even after I provided my insurance information both by phone and via an electronic form prior to my appointment.

In my panic, I decided to look over the bill more closely and used ChatGPT to get insights into what I was actually being billed for.

I quickly found multiple instances of bad-faith billing

The first offender was an oral cancer screening test that I didn't consent to, and that isn't recommended or covered by insurance for patients in my age group.

I was also billed for both a periodontal evaluation and a comprehensive oral evaluation — two services that my insurance would not allow to be billed on the same day because they are so similar. Using AI even helped me by flagging that my 'facial photographic images' were charged at seven times my insurance's allowed rate.

ChatGPT also assured me that it's not standard practice to charge a 32-year-old woman $35 for 'oral hygiene instruction' just because the dental assistant reminded me to brush with my toothbrush at a 45-degree angle.

At first, I addressed my grievances the old school way

I called my insurance company, and the representative validated some of my findings but could only direct me to submit an appeal.

I used Otter.ai to transcribe my calls, then uploaded the transcripts of my calls with the insurance company, the receipt from my appointment, my explanation of benefits, and instructions on how to file an appeal into ChatGPT. In under a minute, it had my appeal letter written.

I did go through five revisions — a couple due to me clarifying certain elements of the experience, one because I didn't like how a sentence was worded, and a couple more because I thought of more information I hadn't previously considered including.

Using AI made the whole process feel less daunting

AI was especially helpful when doing the math on things like co-insurance based on allowable amounts. ChatGPT helped me speak the language of insurance companies and convey my thoughts in an industry-appropriate way.

Plus, it formatted everything according to my insurance company's strict instructions and even provided mailing instructions so I could use as little brainpower as possible.

My first appeal was denied

When my insurance company denied my appeal — because the provider scheduled my appointment with an out-of-network dentist — I wasn't happy, but I did feel more confident in dealing with the issue thanks to ChatGPT. I took pictures of the four-page letter and uploaded them into my previous chat conversation.

ChatGPT summarized the letter and suggested I submit a formal second-level appeal and a complaint to the Arizona Department of Insurance. It also advised that I could contact the dental board for my state, as well as my insurance company's grievance department.

I prompted ChatGPT to draft both the second-level appeal and complaint for me, and I submitted them.

After my second-level appeal, my case was never formally resolved, but the dental office never sent me a bill for what wasn't covered. I believe this is because the office had been contacted by my insurance about the billing issues, and they were aware of my appeals and my complaint to the Arizona Department of Insurance.

Ultimately, I never paid the $1,200.

Using AI made the whole process a lot easier

There's a lot of criticism of outsourcing tasks to AI, and I can understand the argument that the instant fixes it provides can make us less equipped to think critically about our problems. However, I think we've all experienced the dread of opening a piece of mail after a long day and finding purposely confusing language that delivers bad news, a big bill, or both.

I don't see the glory in wasting time and mental energy on tasks like researching dental codes or laboring over formatting. I'd rather save my energy for the things I enjoy, or driving the 45 minutes back to my childhood dental office, where I'm now happily receiving dental services again.

from Business Insider https://ift.tt/uZX57qf

America runs on funny money now

Getty Images; Tyler Le/BI

When Mirav Steckel opened each of her 15 credit cards, she thought the discounts and rewards they offered would save her money. Instead, her plastic portfolio pushed her into impulse purchases and forced her to reevaluate her spending habits.

"If it was a really bad day at work, my first thought wasn't, 'Oh, let me go home and chill.' It was, 'I'm going to go treat myself to something that's going to make me feel better,' but it got to a point where I was asking people around me for money to pay my cards off," Steckel tells me. "That's not the type of life that I wanted to live."

Steckel chalked it up to financial illiteracy — she was 18, she didn't know the crushing consequences of debt, and signing up for the cards was deceptively easy. Now 21, she has a new trick to follow her monthly budget: use cash. Seeing the physical money rather than making a seamless digital transaction has been instrumental to curbing her spending.

Steckel's frictionless financial experience is an example of the cascade of credit card deals, Buy-Now-Pay-Later plans, and digital personal loans designed to grease the wheels of your spending and make it easy to obscure — or ignore — the purchases you're on the hook for. Consumer spending gurus told me that while these products can benefit those who truly need a financial reprieve, they can also trap people in an endless debt cycle that is difficult to escape. And with the risk of renewed inflation and heightened economic uncertainty, some consumers are more willing to enter payment plans, putting less money down up front in the hope that conditions will improve in the future. The Federal Reserve found that 15% of Americans used BNPL in 2025, up from 10% in 2021. That's coupled with 81% of Americans holding a credit card in 2025.

"If I make you wait or if I make you click through a bunch of things or physically pull out a wallet or, God forbid, cash, that will give you all these moments to pause and rethink things," Scott Rick, a marketing professor at the University of Michigan, tells me. "I just want to be a hot knife through butter here. I want to make it as easy and frictionless as humanly possible."

Welcome to the funny money economy, where credit is king and companies excel at making their products so easy to access that you don't stop to think about whether you can actually afford to pay for them.

'It's gotten so easy to spend'

Maybe you know the feeling: You're online shopping, and you only need that sweatshirt, but when you go to check out, there's a $9.99 shipping fee. If you spend $15 more, though, shipping will be free. You don't really need that jacket that you've been eyeing, but if you buy it, shipping is free. It's a steal. Sure, it's a little more than you'd expected to pay, but if you use a BNPL plan, the first installment fits snugly in your budget, and you can manage the other payments down the line. Congrats, you've been sucked into the funny money economy — fueled by the ease of technology and artful tools to prevent consumers from getting a full grasp on their financial situations.

The modern shopping experience is drastically different from what it was even just a decade ago, Abigail Sussman, a marketing professor at the University of Chicago's Booth School of Business, tells me. It's not only the switch from cash to credit cards, she says, it's also the ability to store your card information on the web and automatically fill it in when prompted. Other forms of payment like Apple Pay make it easy "to spend without even looking at the price, frankly, without even really pausing to internalize it," says Sussman. And even if you consider the number on your screen, it may not be the final final cost.

"I don't think consumers are doing anything wrong. I think it's just that the systems that are in place are really designed to make spending frictionless," she says.

These changes also prey on our brain's desire for instant gratification, says Kristina Durante, a social psychologist at Rutgers' business school. Hundreds of thousands of years ago, humans were solely focused on survival — they weren't thinking about what meal they'd have in two weeks. Our brains are still in that mindset, Durante says. While we can think about the future in an abstract way, the human brain doesn't excel at accounting for the future.

"The part of our brain that wants what it wants when it wants it is so much stronger than the part of our brain that's a brake system that says, 'Wait, hold on, can we really afford this?'" Durante says.

Rick, the University of Michigan professor, says that in addition to the ease of shopping, some companies are using entertainment to pull consumers in. He referenced the TikTok shop, where ads for various products pop up in a user's feed while they're watching videos, and people can purchase them with one click. Or take Disney resorts, where a visitor can tap their wristband or use Disney dollars to make a purchase, leading the consumer to feel like they're using "play money" even as their accounts are slowly drained.

'It's hard to keep track'

The mechanisms that make it so easy to spend also make it easy to get access to debt to spend even more. New technology allows companies to instantly approve new customers for credit cards, and there's an expanded availability of specialized cards, like those intended for people with low credit or ones geared toward students with limited credit histories. These lower barriers are helping fuel a record amount of debt. The latest figures from the New York Federal Reserve show Americans' outstanding credit card balances are at a record high of $1.28 trillion, up nearly 6% from one year ago. Over the same time period, the usage of alternative spending, like Buy Now, Pay Later products, has grown — a December 2025 report from the Consumer Financial Protection Bureau said that the six firms in its sample reported a combined 53.6 million consumers who took out a BNPL loan in 2023, a 12% increase from 2022, at an average amount of $848, up from $725.

When it comes time to settle up your accounts, companies are making it confusing to get a handle on where you stand. Credit cards have variable interest rates that can go up or down depending on a range of factors, including credit score. By offering rewards, points, and limited-time low-interest rates, a consumer might not realize what they're signing up for until it's too late, Ayelet Fishbach, a behavior science professor at the University of Chicago, tells me.

"Points don't feel like much," Fishbach says. "And so if you can convince me that I'm not paying with money, but with some monopoly money such as credit card points, that will obscure the price."

BNPL products similarly use smart marketing and our own mental biases against us. Ying Lei Toh, a senior economist at the Kansas City Federal Reserve, says that while they could help some consumers responsibly make big purchases, they are structured to make people feel "less financially constrained" by breaking the cost into installments.

"It could really worsen the overspending problem and the indebtedness, and the possibility that people would really be spending way beyond their means," Toh says. A CFPB report from 2025 found that Americans are taking on BNPL debt more frequently, and at larger amounts, with the average annual loan increasing from $745 in 2022 to $848 in 2023, up 14%. For credit card companies and BNPL providers, allowing consumers the option to split up payments could generate profit because some afterpay plans come with hefty interest rates and late fees. At the same time, the increased availability of these plans helps companies reach a demographic that might not have traditional credit cards or prefers to make payments in smaller installments.

Stephanie Blanks, 35, managed to escape the BNPL trap — but it wasn't easy. When she had her first child about five years ago, she underestimated how much savings she needed. She ended up maxing out her credit cards and turned to BNPL to buy diapers, groceries, and clothes for her baby. Those small, twice-monthly payments turned into about $3,700 in debt.

"You're like, 'Oh, $10 every two weeks doesn't sound bad at all. I can totally afford that,' until you get 25 or 26 loans in and you're drowning in them," Blanks says. She started paying off that balance at the beginning of September 2025 and hasn't used a BNPL product since. "It was just extremely overwhelming, and I felt like I couldn't get out of the hole," Blanks says.

BNPL plans aren't all bad. When Gabby Raines, 29, moved in with her husband about 10 years ago, they needed a new mattress but couldn't afford it all at once, so they turned to a BNPL plan. "It was a total lifesaver," she says. She has since used BNPL to buy a treadmill and clothes, but even as a savvy, experienced buyer, the ease of signing up sometimes causes her to spend more than she intended.

"We live in a world of such instant gratification and overconsumption, which as Americans we are all guilty of, so sometimes we all should take a step back and really look at the consequences of what we feel like we need right now," Raines said.

The serious consequences of the funny money

While being able to push off or spread out purchases can give you freedom in the moment, the expenses can pile up, and you might find yourself months later with dozens of loans and thousands of dollars in debt that you didn't anticipate.

For some consumers, alternative forms of financing are a means of survival. When the pandemic hit, and she lost her job, Susan Cannon, now 73, used her credit cards to pay for groceries, bills, and complete needed home repairs. While it was necessary, it's also come at a steep cost: Cannon is nearly $40,000 in credit card debt and struggling with sky-high interest rates. "I've always tried to put some in savings, but it's gotten to where it's all going toward interest," Cannon says. "So it's like I cannot get ahead."

For many Americans, though, the funny money economy is a means to fuel nonessential consumption. The Bureau of Economic Analysis's measure of personal expenditures, which includes spending on products like apparel and household appliances, stood at $21.4 billion in the last quarter of 2025, up from $19.2 billion in the last quarter of 2023. The keeping-up-with-the-Joneses culture ingrained in American society has fueled overspending, Sussman says. Your neighbors can only see what you're spending — not the giant debt bill on the backend — which can aggravate the tendency to buy more than you can afford when you're constantly comparing yourself to others.

The rise of social media has made that constant comparison a lot easier, Durante says, because instead of comparing our lives with our neighbors, we can compare ourselves with someone who lives across the country, or the world. "Your brain is categorizing someone far away as someone who is a competitor," Durante says. Social media has also turned spending into a joke, with trends like "girl math," a type of mental gymnastics in which someone might justify using a gift card as free money or consider returning an item as a way to make money. But girl math is really just "human math," Durante says, because it's another way that our brain is thinking about the present without accounting for the future.

"We have a brain built for scarcity living in a world of abundance. And there's going to be a lot of poor decision-making that's made because of that," Durante says.

In the worst cases, funny money can lead to long-term strain. Consumers who fall behind on loans could find themselves facing wage garnishment, and their credit scores could take a hit, making it difficult to rent a home or get an auto loan. Bankruptcy filings increased 11% in 2025, indicating that more Americans are turning to the courts as a last-ditch effort to be absolved of their debt. Higher debt loads slow economic growth, as consumers put less money into the economy and more toward paying back what they owe.

The very nature of funny money, though, is that these tough consequences can be under wraps until they come crashing down all at once. And it's unlikely these trends will reverse anytime soon, given pervasive economic uncertainty, Fishbach says. High inflation might lead a consumer to think that it makes economic sense to purchase something now even if they cannot fully afford it, "because the price might be higher later, tariffs might make it higher," Fishbach says. And the existence of mechanisms like debt forgiveness, bankruptcy, and Buy Now, Pay Later products all feed into the funny money mindset, where it's nearly impossible to predict your financial situation a year or even a month from now, making it easier for consumers to put off payments.

"People are smart, but they are busy, and you are not required to get a master's degree in economics before you go to the grocery store," Fishbach says. "We created a system that makes it very hard to make good financial decisions. "

Ayelet Sheffey is a senior reporter on Business Insider's economy team, covering education, student loans, and the federal workforce.

from Business Insider https://ift.tt/6tMYFxa

Sunday, 29 March 2026

Driverless cars, meet your eye doctor

Courtesy Kinetic

- Modern cars are equipped with sensors to support driver assistance systems and safety features.

- Kinetic is a startup that provides sensor calibration after a car is involved in a collision.

- Kinetic CEO Nikhil Naikal said his company aims to service autonomous vehicle fleets.

Human drivers aren't the only ones who need to have eyes on the road.

Many cars on the road today are equipped with at least half a dozen sensors, from cameras to radars, to support safety features and advanced driver-assistance systems (ADAS) that are now ubiquitous in the modern automotive industry. And as automakers continue to offload the task of driving from humans, cars will become even more sensorized.

Kinetic, a Southern California-based startup, wants to scale a service that will fix those sensors if a car ever gets into a collision. The CEO analogizes it to the modern car's optometrist.

"We have eyes, and when we need to correct vision, we go to an optometrist who places all these letters at 20 feet, measures our vision and prescription, and then gives us the glasses to correct our defect," CEO Nikhil Naikal told Business Insider. "In the same way, this is a digital prescription to correct the errors of the car's understanding of the world around it."

No car is the same as it once was after its first fender bender.

Panels get bent, parts are replaced, and the paint won't match the original exactly.

The same principle goes for the sensors on a car, Naikal said. Sensors are highly sensitive to alignment, and a fraction of a degree can significantly affect the effectiveness of an ADAS or self-driving feature.

Once a vehicle is in a front-end collision or rear-ended, those sensors could be thrown out of position. Mechanics can put the sensors back in place, but they won't be re-mounted in a spot perfectly identical to their factory placement.

That's where Kinetic's robotics platform and software come in to calibrate the sensors — or, as Naikal put it, give them a "digital prescription."

The auto shop of the future

An 8,000-square-foot facility in San Francisco's Dogpatch neighborhood is one of eight Kinetic hubs on the West Coast.

The inside is unlike loud, messy auto body shops. A Kinetic facility is quiet and mostly empty save for a rotating platform and a robotic arm attached to a short track. A typical location is staffed with up to two technicians, Naikal said.

On a Wednesday afternoon, Kinetic was servicing a 2022 Toyota Camry Hybrid LE that had been repaired at a local body shop after a front-end collision.

Lloyd Lee/BI

The car was driven onto the platform, where Kinetic's camera package takes detailed photos of the car, and a robotic arm points a laser at the radar sensor embedded in the Toyota's grill.

Kinetic's software then puts the car and the sensors back in sync.

"What the car thinks it's going to do and what the sensors think the car is going to do needs to be aligned," Naikal said. "The sensor thinks that the car is going to go right, whereas the car actually needs to go left — that's a problem. It causes unstable things like ghost braking and jerking."

The entire process takes about 10 minutes. Naikal said a single Kinetic hub can service about 80 cars a day.

Some repair shops might rely on a mobile service, in which a specialized technician comes to calibrate the sensors. Naikal said a lot of body shops don't have the space, lighting, equipment, or trained technicians that can accommodate an in-house service. Local body shops can either choose to send cars to Kinetic's hub or, if they have space, lease the company's equipment.

By the end of 2026, Naikal said he aims to have 20 hubs in the US.

Kinetic's platform can also perform damage inspections and develop repair plans, but Naikal envisions servicing autonomous vehicle fleets, which require constant cleaning and sensor maintenance, as another line of business. The future, he said, will require a new kind of service infrastructure built around robotics and software rather than a traditional body shop.

"It's going to be more than just Jiffy Lubes and Valvolines," Naikal said. "We think of ourselves as the infrastructure layer for the future of autonomy."

from Business Insider https://ift.tt/zI4H8CA

Saturday, 28 March 2026

China's 'one-person companies' have exploded. An Alibaba exec explains how AI agents make that possible.

Horacio Villalobos#Corbis/Getty Images

- Alibaba.com president Kuo Zhang says AI is aiding the surge in one-person companies.

- OpenClaw, an AI agent, has helped boost the trend in China.

- Alibaba.com faces tariff-related challenges. Zhang says he focuses on two things to navigate them.

China has seen an explosion in "one-person companies" thanks to a little help from AI agents.

Alibaba.com president Kuo Zhang told Business Insider he has seen this growth firsthand, estimating that 30% to 40% of the e-commerce platform's customers are "solo entrepreneurs."

Business Insider previously reported on the rise of one-person companies, or OPCs, which rely on AI tools such as agents and vibe-coding technology to build their businesses without hiring other employees. Some Chinese cities are attracting these startups by offering free housing, rent-free offices, and subsidies of up to $720,000.

Zhang said AI agents have helped make these types of startups possible. He runs Alibaba.com, the Chinese cloud and retail giant's e-commerce platform that connects buyers and suppliers. While most of its customers are from China, it's also growing its customer base in the US, Europe, Latin America, Southeast Asia, and other regions.

One-person companies face barriers to building their business. Tasks like uploading products to different sites, managing social accounts, and handling customer complaints are "easy for a big company" but harder for small businesses, Zhang said. While these tasks may not be the expertise of small businesses, they are "essential for success," he added.

Agents can help with some of that grunt work.

"Instead of taking the place of the human beings, actually, they are the employees of that solo entrepreneur," Zhang said of AI agents.

Alibaba.com recently launched Accio Work, an AI agent designed for small businesses, including one-person companies. It can help companies manage daily e-commerce operations, including customer service, tax compliance, marketing, logistics, product listings, and more.

"They are in lack of help or tax support. And now, AI is very easy to use. It's very easy to adopt and to understand everything is going to change that perspective, and we think they can benefit from them the most," Zhang said.

Alibaba.com's main Accio agent first launched in late 2024 and now has 10 million active users a month, according to the company.

China's OpenClaw craze

The rise of OPCs has been boosted by OpenClaw, the open-source AI agent that has become wildly popular in China. The craze has sparked a sort of OpenClaw gold rush and spawned quirky agents for stock trading and setting up blind dates. Many OPCs have also built businesses using the OpenClaw agent.

Zhang says that the rise in OpenClaw has helped educate the market about AI agents. Alibaba itself introduced JVS Claw, a mobile app to help users install and deploy OpenClaw more easily.

Compared to China, Zhang said American users are less educated about OpenClaw and that there's a smaller scene around it. That said, OpenClaw has issues with security and return on investment, he said, adding that some customers have spent "hundreds of US dollars for tokens," and when they don't get the results they want from using agents, they quit.

Instead, it's important for agents to be user-friendly, secure, and easy for customers to get started, he said.

"If you go to SMBs, you ask about all the fancy terms about AI, like the token economy, like cloud, like open cloud, probably they've never heard about that, and what they care most is about how these tools can help me," Zhang said.

Alibaba faces changing tariff policies

Alibaba.com and businesses on the e-commerce platform face another major challenge: navigating a constantly changing tariff landscape. Zhang first became president of Alibaba.com in 2017, during President Donald Trump's first term. As policies change, Zhang said it helps to focus on two things: serving customers based on supply and demand, and technology.

"Technology changes on a daily basis, so I've learn a lot from the tech companies, and from our SMBs. They will tell us what they need and how we can leverage tech the best to help them on a daily basis," Zhang said.

"The rest, I say, is noise," he added. "Just follow all the rules, and we follow all the rules in the world."

Have a tip? Contact this reporter via email at rmchan@businessinsider.com, or Signal at rosal.13. Use a personal email address, a nonwork WiFi network, and a nonwork device; here's our guide to sharing information securely.

from Business Insider https://ift.tt/spZ5yqn

'Informed' traders on Polymarket netted $143 million in 'anomalous' profit since 2024, researchers find

Bloomberg/Getty Images

- "Informed" Polymarket users made $143 million since 2024, according to a new study.

- Researchers analyzed most of Polymarket's trades between 2024 and 2026.

- One co-author told BI he hoped the analysis would inform prediction-market regulation.

Last June, a new Polymarket account with the name "ricosuave666" began betting thousands of dollars on specific questions regarding Israeli military strikes on Iran.

The gamble paid off. When Israel struck Iran in the early hours of June 13, ricosuave666 pocketed roughly $155,000 before going dormant for seven months. The account resurfaced in January 2026 to place new wagers — before analysts flagged its activity and it was promptly deleted.

Ricosuave666's moves were among more than 210,000 suspicious Polymarket trades analyzed by researchers at Columbia Law School and the University of Haifa. The trades netted $143 million for the "informed" traders who made them, according to the researchers, whose findings were published this month.

The most suspicious trade made by ricosuave666 was only the 3,662nd-most unusual trade in the data, authors Joshua Mitts and Moran Ofir wrote. They said ricosuave666's gains closely matched ill-gotten gains attributed to a person charged by Israeli authorities with using military secrets to trade.

The study, which analyzed most of Polymarket's trades between 2024 and 2026, is the first to provide an estimate for the total amount won by suspicious accounts, whose activities are often flagged by market observers and traders on X and Discord chats.

The authors used five criteria relating to trade timing and amounts wagered to screen for accounts that made big, bullish bets shortly before news broke, though they acknowledged that their methods could have been over-inclusive or under-inclusive.

"We don't have any reason to think that the unobserved relationships are cutting in one way or another," Mitts, a Columbia Law School professor who has previously written about potential insider trading in equities markets, told Business Insider.

Mitts told Business Insider that he and Ofir generally used the term "informed" trading rather than "insider" trading because some of the biggest trades they flagged took place in markets where too many people influence the outcome for it to be rigged, like those related to Donald Trump's 2024 election. "Informed" is a broader term that encompasses trades made by smart bettors as well as those with unfair advantages.

The study said the election bets were included with other "anomalous" bets because the authors didn't want to be accused of massaging their methodology to get a particular outcome.

"We think there's going to be a lot of regulatory attention. We see this as just the beginning of the conversation," Mitts said.

No proof of insider trading

The authors said it's possible that they flagged profitable trades that were part of a hedging strategy and offset by a loss in another wallet controlled by the same user. Still, they characterized the volume of suspicious trades they identified as a "conservative lower-bound estimate of anomalous profits."

Harry Crane, a Rutgers statistics professor who has written about prediction markets and was not involved in the study, questioned its methodology. While the study ranked over 210,000 bets based on how unusual the bets were for the traders who made them and for the markets where they were made, the ranking of their "suspiciousness" was heavily skewed by profitability, rather than what ordinary people would consider suspicious, he told Business Insider.

"A winning bet is getting disproportionately more weight than a losing bet of the exact same type," Crane said.

Most of the 20 most suspicious trades identified in the paper, accounting for about $16 million of the $143 million in profits reaped by flagged accounts, related to the 2024 election results. Others related to Federal Reserve decisions and sports match-ups, where manipulation is theoretically possible or insider information theoretically could have leaked.

Mitts said the plan was eventually to publish all the data used for the study.

"Prediction markets have outpaced the legal frameworks designed to govern them," the authors wrote. "Our paper aims to provide the empirical grounding and legal analysis necessary to close that gap."

Polymarket changed its policy

Prediction markets have been around for decades, initially as academic experiments and later as a tool popular with members of the so-called rationalist community. The general idea is highly accurate guesses about the future can emerge from a group of non-experts who put their money where their mouths are.

Some advocates for prediction markets see insiders cashing in as a feature, not a bug. Shayne Coplan, Polymarket's founder, said last year that it's "cool" that Polymarket "creates this financial incentive to divulge information to the market."

Earlier this month, the company announced that it was banning trades by people with "stolen confidential information" and "illegal tips" as well as trades by people who can influence the outcomes of events they're betting on.

It's not clear how the company will enforce the prohibition when it doesn't know who its users are. While the company has a regulated US subsidiary, that entity processes less than 10% of the volume of trades as the offshore exchange, which doesn't collect users' names or other identifying information beyond an email address.

It didn't reply to requests for comment from Business Insider.

Kalshi announced earlier this year that it is seeking fines from two users who broke its rules, including a video editor for MrBeast who placed bets on what words would be said on shows before they were released.

Prediction markets grew slowly for years. In 2025, Kalshi grew rapidly after it began offering Americans the chance to bet on sports in a way it calls more fair than sportsbooks. Problem gambling experts are concerned that prediction markets pose similar risks to sportsbooks, however, and several states have sued Kalshi and other prediction markets, arguing that they amount to unlicensed casinos.

The Commodity Futures Trading Commission, a federal regulator, fined Polymarket in 2022 and generally prevented prediction markets from offering many contracts until Trump took office last year.

Michael Selig, a Trump appointee who took the helm of the regulator last year, has been a vociferous advocate for such markets, and criticized the states for their crackdowns.

Have a tip? Know more? Reach Jack Newsham via email (jnewsham@businessinsider.com) or via Signal (+1-314-971-1627). Use a personal email address, a nonwork device, and nonwork WiFi; here's our guide to sharing information securely.

from Business Insider https://ift.tt/6wX8TgR

Friday, 27 March 2026

The king of love: How Spencer Rascoff reshaped Tinder — and our dating lives

Bloomberg/Getty Images

- In just over a year, Spencer Rascoff has radically transformed how Tinder operates.

- Rascoff changed up the org chart, pushed back on narratives of fatigue, and recentered on what Gen Z wants.

- He told Business Insider about his leadership — and why a long-married man would want to run a dating company.

Spencer Rascoff met his wife before Tinder. And eHarmony. And Match.com.

He was 17 years old, attending a barbecue for students who planned to attend Harvard College. They got to Cambridge, started dating, and have been together since. His next love-match was startups, founding a slew of tech and media companies, including his opus, Zillow.

Then came Match Group, the conglomerate that owns apps like Tinder and Hinge. He knows what you're thinking: What qualifies this long-married man to know what singles want? He's never had a Tinder hookup gone wrong; he's never longed for those in Hinge's rose jail.

"I am living proof of how important it is to find the right person," he told me at Match Group's sunny West Hollywood office. "Were it not for her, it would be awful."

Rascoff thinks you can find that same life partner on his apps. The market seems to disagree, with stocks down across the category in recent years. In the post-pandemic dating app boom, Match Group's stock traded around $150; now, it hovers around $30. Five days before I spoke with Rascoff, the S&P 500 announced that it would expel Match Group.

Rascoff needs to make online dating sexy again. He's done it before — think of how stuffy the homebuying process was before Zillow. But Zillow was a disruptor, where Match Group is a legacy player. It'll take bigger swings to get more Americans swiping right.

Inside Rascoff's Tinder redesign

Rascoff doesn't come across like the stereotypical "founder mode" type. He's calm and quiet-spoken, often stopping mid-sentence to consider exactly what he wants to say.

Power centralized around Rascoff soon after he joined Match Group. He took over as CEO of Tinder from Faye Iosotaluno. Two of Match Group's longest-standing faces have also since left: Hinge founder Justin McLeod and chief operating officer Hesam Hosseini. The COO position will not be refilled.

Rascoff quickly reformed Tinder into a series of independent pods. He subscribes to Amazon's two-pizza rule: a team should never be so big that they'd need more than two pizzas. He also made the company flatter. It put Tinder in line with how he ran Zillow and how Hinge was already running, he said.

"Tinder product and engineering used to be a very large, monolithic organization where the priorities of what gets built came from on high," he said. The org chart change "unleashed an enormous amount of innovation that was buried."

He also drilled into the app's mission statement: "Tinder is the most fun way to spark something new with someone new." The team now says it in unison before every company meeting, something Rascoff said he values, even if it can be "awkward" and "creepy."

Henry Chandonnet/Business Insider

Multiple Tinder leaders told me that the dating app now runs more like a startup. (Two leaders directly used the term "founder mode.") It's an ironic twist, given that Tinder itself was born in a conglomerate: IAC's Hatch Labs. But Rascoff seems bent on ripping up any remnants of bureaucracy.

Right before the team went on stage at the Tinder Sparks conference, Rascoff approached Claire Watanabe, Tinder's vice president of product. He was using the new Music Mode, and wanted to know why he couldn't hear it on his profile, she said.

"He's into the details," Watanabe said. "He has an opinion."

Navigating a sour dating app market

Rascoff and I mostly abstained from talking about Hinge. Part of that is because of the event: We're here for Tinder Sparks, a moment when Rascoff can play Steve Jobs to talk about a litany of new features.

The other reason, though, is that Hinge is doing really well.

Hinge is "on a path to be a billion-dollar business," Rascoff said. "The way they've done that is by knowing whom they're building for, and by bringing consumer insights into what they're building."

Tinder, on the other hand, has slumped. Its annual downloads have been shrinking since 2023, according to Appfigures. In 2021, 61 million people downloaded Tinder, the firm found. In 2025, that figure dropped to 48 million downloaders. Meanwhile, Appfigures found that Hinge was consistently showing positive growth in annual downloads.

Make no mistake: Hinge maintains a fraction of Tinder's user base, and Tinder is still the biggest dating app in the world. But the warning signs are certainly flashing as red as a Tinder flame.

The Tinder Sparks event was a moment to turn it all around. Rascoff spoke confidently on stage, looking casual in his blue jeans, and outlined a vision for the future of dating. We sipped oat milk lattes and smiled for the photo booth. It's hard not to be excited about an app when it's named in a Bad Bunny song.

Henry Chandonnet/Business Insider

The room's optimism didn't seem to match Tinder's perception in the outside world, where we hear constantly about "swipe fatigue" and the decline of online dating. Women especially report low-quality matches; a 2022 Pew study found that more women reported negative than positive online dating experiences.

When I asked Rascoff about fatigue, he chose his words carefully. "Some people have left the category because they find dating apps tedious," he said. His goal is to introduce "fun" features to combat that feeling.

M Science research analyst Chandler Willison said that some investors have begun to think that those worries — about "systemic issues" and "industry-wide malaise" — weren't as unchangeable as they once believed.

"Spencer has done a really good job pushing back against that idea," Willison said.

A new generation of daters

Rascoff may be married, but he's still swiping.

He excitedly showed me his phone. His Tinder profile had a photo of him, his wife, and his dogs. His bio says that he's "just here for research about our product."

It's not his first go-around on the apps. A few years after his father died, Rascoff's mother got on the apps. He served as his mother's "dating copilot," helping her improve her profile and respond to messages.

For Tinder to bounce back, he'll have to aim his dating advice down a generation. Rascoff talks about Gen Z constantly. He went directly from Match Group's Gen Z employee resource group to our interview, he said. He cracks jokes about Gen Zers who bring up astrology in their job interviews, and shows off a Rubik's Cube with Tinder's imaginary Gen Z customers.

Henry Chandonnet/Business Insider

Match Group isn't the first company to prioritize Gen Z. It's why Nespresso brought in Dua Lipa, and why the Duolingo owl raved to "brat." For Match Group, though, the generation is life-or-death. You might still need espresso or a language app when you're 45 and happily married, but you won't need Tinder.

I'm a Gen Zer myself, a 23-year-old Tinder swiper. It was an odd experience to sit in the Tinder Sparks auditorium and be told by older generations how I want to date. I want to be "perceived authentically," they said. I'm interested in "self-development," they said.

During our interview, Rascoff reminded me that Gen Z wants "lower pressure" ways to date. That's why they pivoted to in-person events; because they're chill, and because they're "meeting Gen Z users where they are."

The low-pressure model made sense. I'm not dating for marriage; I just want to have a good time. But why, then, are all my friends on Hinge, the higher-pressure alternative? (Hinge lets you like fewer people, and doesn't provide the anonymity of a two-way match.) I could name at least four Gen Z couples in my life who met on the app designed to be deleted.

For a while, all I heard about Tinder was that it was an endless hole of one-night stands. Then, I met up with a friend, who told me that she'd started dating. She let me in on a secret: it wasn't Hinge she was using, but Tinder. It was easier, she said.

There's little real data to back up a Tinder turnaround yet. Monthly downloads remain at about 3.9 million and haven't started climbing, per Appfigures. Willison said that Tinder was still in a "recovery" phase. But my friend's confession felt like a sign. People can (and do) still find sparks on the app.

Rascoff said he thinks he'd do well on Tinder. Those who are authentic and put in the hours find their spark, he said. "If I were single, I would certainly do that."

from Business Insider https://ift.tt/lhqnTy5

Thursday, 26 March 2026

Silicon Valley investor Ron Conway says California's proposed wealth tax 'could' pass if it's up to voters

Jeff Chiu/AP

- Tech investor Ron Conway is worried that California's proposed wealth tax could pass.

- He and several other big names in tech are funding campaigns to stop the proposed ballot initiative.

- Conway said it's imperative that the proposed tax never reach the ballot.

Famed Silicon Valley investor Ron Conway says he wants to kill California's proposed wealth tax now.

"Our job is to get Gavin to negotiate this so that it doesn't get to the ballot. So, maybe they don't get the signatures," Conway told Jack Altman during an episode of Altman's "Untapped" podcast that was posted on Wednesday.

Conway, the founder of SV Angel and known as "The Godfather of Silicon Valley," said that if the proposed wealth tax reaches the ballot, it "could" pass.

A recent UC Berkeley Citrin Center for Public Opinion Research-Politico poll found that support was hovering around 50%, within the margin of error of potential failure, though it is still very early in the process.

Major names like Google cofounders Sergey Brin and Larry Page have already rushed to move assets out of California, the state home to the most billionaires. If passed, California residents with a net worth of over $1.1 billion would face a one-time tax totalling 5% of their assets. Supporters of the initiative are still gathering signatures ahead of a June deadline.

Conway said Gov. Gavin Newsom, who is publicly opposed to the wealth tax initiative, is aligned with the efforts. Conway said one way to give Newsom bargaining power is by supporting the three competing ballot initiatives, which would effectively neuter the proposed wealth tax.

Brin, Stripe cofounder Patrick Collison, former Google CEO Eric Schmidt, and others have poured over $44 million into "Building a Better California," a political action committee that is pushing the three competing anti-wealth tax ballot measures. In November, Conway donated $100,000 to "Stop the Squeeze," another group that is opposed to the proposed tax.

Venture capitalist Marc Andreessen once called Conway "the human router," a nickname he told Altman that he considers a compliment. Conway has been a fixture in tech for decades, making early bets on Google, Facebook, and other companies. OpenAI CEO Sam Altman, Jack's brother, credited Conway with helping him hold OpenAI together during his brief ouster in 2023.

Conway also told Jack Altman that their interview could not run late, because that night he had courtside seats at the Golden State Warriors game next to House Speaker Emerita Nancy Pelosi and her husband Paul.

"We must keep this off the ballot," Conway said. "So a whole bunch of work has to happen for that."

from Business Insider https://ift.tt/tjmN4T1

8 travelers told us how they fared in the great TSA toss-up of 2026

Michael M. Santiago; RONALDO SCHEMIDT / Getty Images

- Getting through airport security in the US is like playing roulette right now.

- Some travelers are missing flights after hours in line, and having to spend the night in the airport.

- Others are budgeting hours for TSA chaos — and then sailing through the line in minutes.

Bazela Malik was in New York City to celebrate Eid with her family. Her journey back to Fort Lauderdale turned into a more than 24-hour ordeal, involving two missed flights, several Ubers, a walk in the rain, and a sleepless night.

She is one of millions of people who have endured nightmare travel days as the partial government shutdown has thrown US air travel into chaos.

But not all chaos is created equal — and more than a month after TSA agents started calling out of work due to missed paychecks, disrupting the flow of travelers through airports, passengers are playing an unwelcome game of roulette.

Some are arriving at the airport hours early, only to find minimal delays and to breeze through security. Others are waiting for hours in snaking queues only to miss their flights.

One of the problems at play is that it's been nearly impossible to predict which airports will have long lines, and when. TSA callouts at some major airports have been as high as 40%, resulting in major disruption; Atlanta and Houston George Bush airports have both warned of 4-hour delays for days. Other airports, meanwhile, have been able to keep operations running more smoothly — Las Vegas Harry Reid Airport, for instance, has seen minimal lines.

As a result, many travelers don't know how early to show up at the airport. Further complicating matters, hubs like JFK, Newark, and Atlanta have suspended real-time TSA wait-time tracking on their sites. The My TSA app, while spiking in downloads, is not fully functional during the partial government shutdown.

"The uncertainty and lack of reliable information" was the "worst part of the experience," Cora Bravo, a journalist who flew from New York to Mexico City on Tuesday, told Business Insider.

"The official wait times didn't match reality, and people in line didn't really know what was happening or how long it would take."

Chaos in the TSA line — sometimes

Malik's nightmare trip began when she missed her JetBlue flight from LaGuardia on Sunday evening because she was stuck in a three-hour security line. Her next flight, around 6 a.m. on Monday, was canceled because of the Air Canada plane crash that led to LaGuardia being shut down.

Unable to get a taxi at LaGuardia, she walked in the rain to a pickup spot, caught a cab to JFK Airport, waited for six hours at the airport, and finally caught an afternoon JetBlue flight back to Fort Lauderdale, where she works as a hotel accounting manager.

"When you go on break from work, you just want to relax," she said. "But the whole experience made me feel very stressed out."

Many airports are facing staffing shortages as more Transportation Security Administration agents call out of work. While the shutdown began on February 14, the situation was exacerbated when TSA agents missed their first full paycheck earlier this month.

While Republicans want billions more in funding for the Department of Homeland Security, Democrats want to see reforms of Immigration and Customs Enforcement, following January's violence in Minnesota.

Friday is a key deadline. Not only does it mark another missed paycheck for TSA staff, but it's also the last day Congress is scheduled to be in session before a two-week break.

'The line was eating itself'

For New York-based advertising copywriter Megan Walsh, the TSA chaos came at a really bad time.

Stuck in the TSA queue at LaGuardia before her flight to New Orleans for her sister's bachelorette party on March 18, she got a call from her company's HR and CEO, who informed her that she had been laid off.

"My legs were shaking because I was so scared about the call, and I couldn't get through the line in time," Walsh said, saying it was a terrible time to get the news.

Laura Rozner

The bachelorette trip was a good distraction for her, she said, but the travel chaos picked back up when it was time to head back to NYC on Sunday. Arriving at the airport more than four hours before her American Airlines flight, the staff pointed her and her friend Laura Rozner to the garage, where the queue began.

Laura Rozner

"You know the game, 'Snake?' It was like that — the line was eating itself," she said. "We couldn't figure out where the end of the line was; there were loops and loops of people."

Rozner, a marketing manager based in NYC, said she didn't think to pack food or drinks. By the end of the four-hour wait, she was hungry and stressed. She made it to the gate 30 minutes before boarding.

Madison Terry, a small-business owner from Atlanta who was traveling to Florida with her 1-year-old twins on Delta Air Lines on Saturday, said she'd never been so anxious on a travel day.

"There were moms who had to ask people to hold their spots so they could get water for their babies, older gentlemen with canes who had to pee, a student crying because she'd missed her exam," Terry said.

Rebecca Bendheim, an author from Austin, said she was traveling to Colorado with her fiancée for a family ski trip. Their journey was so delayed that she said her family of 14 gave them a standing ovation when they finally arrived.

Rebecca Bendheim

Others are cruising through airports

Some travelers managed to strike the TSA lottery.

Shayna Macklin, an NYC-based marketing director, said she arrived at JFK five hours early for her Delta Air Lines flight to Nevada because she expected to wait in line.

Macklin, who said she has TSA PreCheck Touchless ID and CLEAR, said she got through security in three minutes.

"I absolutely expected to be waiting in line for hours," she said.

"I will say that I did feel a bit uneasy, but was grateful that I had a good experience going through security and that my flight left on time," Macklin said.

Abby Cox, a teacher from Alabama, arrived seven hours before her flight from Hartsfield-Jackson Atlanta International Airport on Tuesday. While the airport warned of four-hour lines, she said she got through in under 45 minutes.

"I have a medical condition where I cannot hold my bladder, so I was very anxious about the bathroom situation," Cox said. "I consider myself very fortunate to have gotten through so quickly, and I had no problem waiting at a gate for 6 hours."

ICE agents in airports and airline CEOs losing patience

With scores of TSA agents not showing up for work, the DHS has deployed ICE agents across 14 US airports to fill some of the gaps. ICE agents aren't doing any of the TSA's key security screening work, but have been managing lines and directing passengers.

Flight attendants' unions have slammed this step. "TSA workers must be paid now," they said in a joint statement Sunday.

Airline CEOs are losing patience, too. Earlier this month, they signed a letter from the Airlines for America trade group that called on political leaders to "immediately" reach an agreement. "Then they need to act so this problem never happens again," it added.

"Once again, air travel is the political football amid another government shutdown," the letter said.

United Airlines CEO Scott Kirby, one of the signatories, also told CBS News: "It's just ridiculous to me that it has to get bad before they can get a deal done."

"Please get the deal done soon."

from Business Insider https://ift.tt/pga2cxi

Wednesday, 25 March 2026

Tuesday, 24 March 2026

He applied to 1,600 jobs. He finally got one, but it came with a 50% pay cut

Getty Images; Alyssa Powell/BI

Since losing his job in 2023, Scott had applied to 1,600 jobs, completed 78 interviews, and depleted his savings just to stay afloat. The constant rejection had become so unbearable that he went on antidepressants. So when a recruiter from a staffing company called with a job offer last December, he hung up, walked upstairs, told his wife the news, and cried. "It finally happened," he remembers thinking.

The triumph, though, was bittersweet. The position was a six-month contract as a technician, two steps down from his previous role as senior manager. He'd have no guarantee of work once the contract ends. And he'd be earning only half what he made before. "Accepting this is going to set my career back five years," he told me. "I know I'm really good. I want a chance to prove myself."

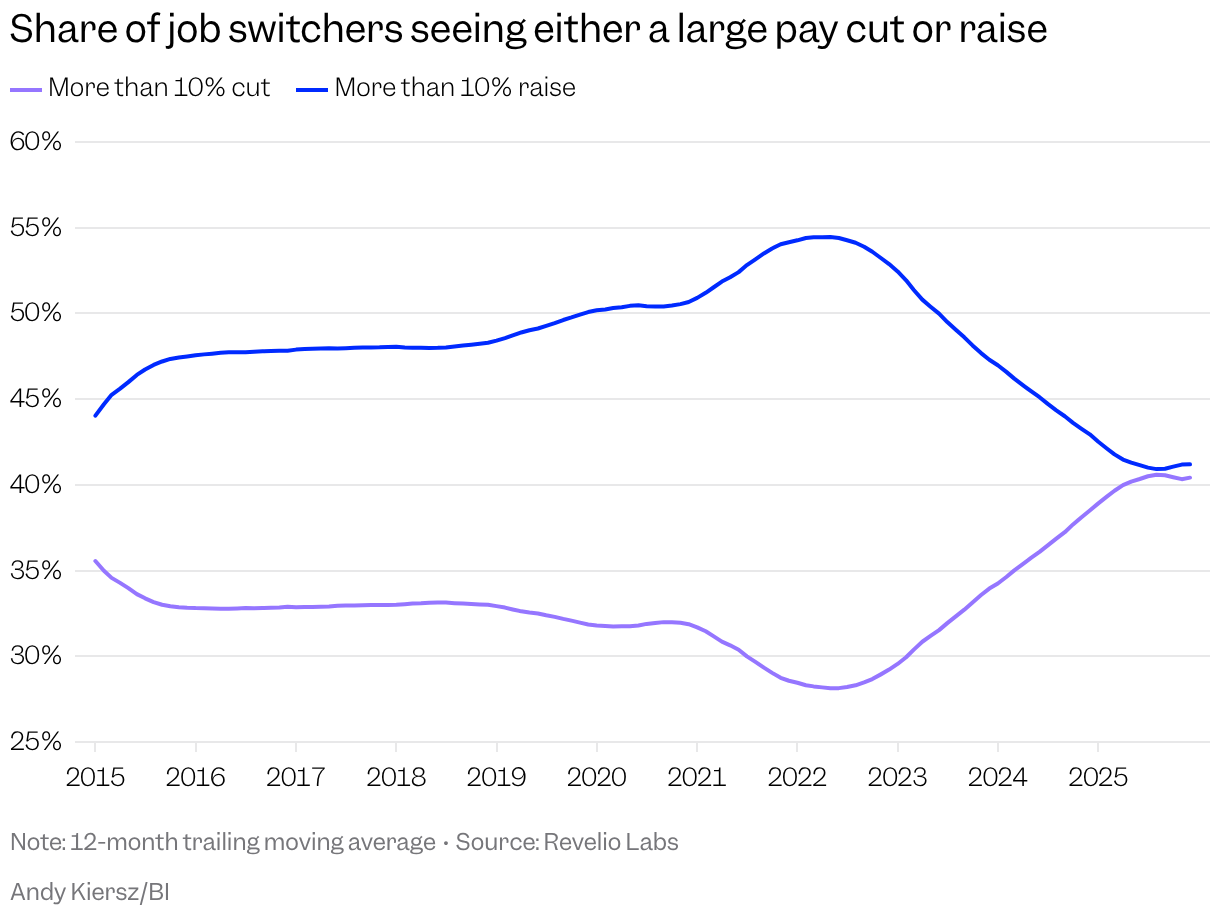

We've all heard about how grueling the white-collar job search has become. But the market is so tough right now that even the people landing jobs often aren't the success stories they appear to be. Revelio Labs, an analytics provider, recently looked at the data it collects from across the internet, and found that an alarming share of people are settling for roles that pay less than the ones they had before.

Among all white-collar workers who changed jobs at the end of last year, 40% took salary cuts of more than 10%, Revelio Labs' analysis showed. That's the highest share in at least a decade. The share of professionals getting similarly large raises is also at its lowest level.

The finding suggests the labor market may be weaker than it appears. Only 4.4% of the US workforce is unemployed — low compared to historical averages — but that may be masking how hard it's been for the people who've lost their jobs to find new ones. For example, the number of people who've been unemployed for at least 6 months — considered long-term unemployment — has nearly doubled over the last three years, according to government data. After protracted searches, people like Scott are accepting jobs they couldn't have imagined taking at the outset.

Workers are taking these pay cuts because companies just aren't hiring much right now. In December, when Scott accepted his job, he was one of 7.5 million unemployed Americans competing for 6.6 million job openings.

Because of that imbalance, employers have gotten pickier about who they hire. One way that's showing up is in job postings. Companies are requiring more years of experience for their open positions, Revelio Labs' analysis shows. That's been especially true for mid-career roles that now ask for 10% more experience than they did three years ago, and senior roles that ask for 11% more.

All of that could have lasting consequences for workers like Scott. If he stays at his current company, future raises will start from a low base; if he interviews elsewhere, employers will anchor their offers to what he's likely making right now. By taking the pay cut that he did, he risks earning less for years to come — a phenomenon economists call wage scarring. But with the job market so weak, the bigger risk for him was probably staying unemployed.

The best hope of minimizing that scarring is a rebound in the white-collar job market. So far, that hasn't materialized; if anything, things are getting worse. Companies from Block to Atlassian have cut staff in recent weeks in moves they attributed to AI, and Meta is reportedly preparing to eliminate 20% of its workforce — a decision that would flood the market with about 16,000 additional unemployed tech workers. In February, the US economy unexpectedly lost 92,000 jobs.

For now, Scott is doing what he can to impress his new bosses. He's already making some headway: He's up for a promotion at his company that would come with a small pay bump. He's also interviewing for a couple of roles with other employers that would come with an even bigger increase.

He's not holding his breath — after so many rejections, he doesn't want to get his hopes up — and none of the roles would get him back to his pre-layoff salary. But any one of them would get him a little closer to the career path he was once on. "I know I can impress people if they give me a moment," he says.

Aki Ito is a chief correspondent at Business Insider.

from Business Insider https://ift.tt/zN6KWeh

Monday, 23 March 2026

Sunday, 22 March 2026

Gen Z is feeling nostalgic for a life they never knew

FX; Getty Images; BI

- FX's hit show "Love Story" offers a nostalgic glimpse of 1990s New York romance.

- Gen Z's fascination shows a longing for pre-Internet simplicity and connection.

- Nostalgia-driven trends have risen as Gen Z seeks comfort and inspiration through analog moments.

Early in FX's hit show "Love Story," an extraordinary scene takes place.

John F. Kennedy Jr. rolls up on his bicycle to meet Carolyn Bessette for their first date. She's strolling out — she tells him he could've called the restaurant to let her know he was running 20 minutes late.

It's a simple moment, but one that feels unthinkable today, when they might have exchanged dozens of logistical texts, or she would've sent frenzied back-and-forth messages with friends debating if he's ghosting her or not. As a late 20's dater in New York City, it was like watching a slightly alien, distorted version of my own reality: A New York City with some of the same long-standing restaurants and subway stations, but marked by a very clear absence — not a phone in sight.

While not the Stone Age, the '90s low-tech life is part of the show's appeal to other Gen Zers and me. Since many of us don't remember the '90s — if you look across the Hudson to Brooklyn in the series, you can see me being pushed in a stroller — it's all a beautiful fantasy of an analog life we'll never know.

Clay Routledge, a psychologist who has written about and researched nostalgia and leads the Human Flourishing Lab at the Archbridge Institute, said the bittersweet feeling can transcend our own memories. In his research, he's seen younger generations report high levels of nostalgia for a pre-Internet past they never inhabited. Art, photos, movies, books, and TV shows can help create a collective nostalgia — look no further than Gen Zers devouring shows like "Friends." It's comforting; we use it to reassure ourselves or to find inspiration and wisdom, Routledge said. That's true even when we reminisce about moments that we haven't lived through.

"It turns out people can do that not just from their own memories, but from sampling the shared cultural memories and experiences in a variety of ways, from talking to people, talking to older generations and hearing their stories, to watching TV or film," Routledge said.

The obsession with "Love Story" — which has broken streaming records for FX's limited series and already sparked lookalike contests — might also be a sign of the times. We turn to nostalgia when the present seems uncertain; in a time riddled with AI anxiety, skyrocketing costs, and increasingly online social lives, it makes sense that Gen Zers might seek solace in a '90s New York that's more Kodak than iPhone.

"One common theme that comes up a lot is feeling overwhelmed or distracted or pulled in lots of different directions with these technologies," Routledge said. Moments like that first date of the leading couple show a level of intentionality and trust that's harder to come by in a world awash with technological options and choice overload.

"There seems to be a real thirst to make things more human-driven and less augmented by technological assistance. And again, I don't think that's because people are like, 'Oh, the technology is bad,'" Routledge said. "It's more like, at some level, we want to get to the point where the technology is almost in the background, and it can be human to human again."

What nostalgia tells us about how Gen Z hopes to shape the future

As often happens with any generation, Gen Zers are soothing their anxiety with consumption — the plastic headband Bessette wears, for example. Nostalgia and analog-based products and marketing have exploded over the last few years, and "Love Story" is no exception. Ashley Bauchman, a 34-year-old producer and creator in Los Angeles, sees a sublimation of Gen Z's desire for community. Buying a headband means feeling like a part of a group, but it's still an imitation of the real thing.

"When I find myself spiraling on, 'oh, I should buy this thing, or I should get these clothes, or I need to revamp,' one of the main things that works the best is just taking a pause and thinking to myself, when is the last time I hung out outside with one of my friends?" Bauchman said.

She's noticed that among some of the Gen Zers she encounters online, there's a tendency to be almost self-isolating, opting to "protect their peace" or go to bed early rather than socialize. To be a part of a community or adopt a more analog lifestyle, you have to be willing to inconvenience yourself a bit.

Of course, no headband will throw Gen Zers back in time, or scrub away cellphones. Externally, the economic factors that allowed New York City denizens to live downtown or afford more nights out are far gone. In 2000, the median gross rent was $705 in New York City, which would come to around $1,288 in 2024 dollars. That's well below the actual median gross rent of $1,811 in 2024.

The Gen Zers who love to fixate on a pre-Internet past don't want to throw all technology into the Hudson. The ravenous response around the show might instead point to a certain hunger from the next generation of adults. Look no further than the rise of analog bags, anti-social media events, and the Gen Z desire to pick up tactile hobbies.

"A lot of young people are saying the future we want is a future where technology is present and continues to make our lives easier, but where we are more present, where we're not just passively staring at screens, where we're actually engaging in the world," Routledge said. "So it seems to me that Gen Z is more motivated to not reverse digital technology, but to build the future in which that technology takes a backseat."

from Business Insider https://ift.tt/ImCx7Ey

Saturday, 21 March 2026

A dietitian lost 20 pounds while enjoying her favorite foods by following her simple 'PPP' rule

Hailey Gorski

- A dietitian created a simple template that helps her build balanced but enjoyable meals.

- Hailey Gorski anchors her meals in satiating protein and micronutrient-packed fiber.

- She focuses on what she can add to her plate rather than what she can remove.

Hailey Gorski has a simple rule for making delicious meals that fit her nutrition goals: PPP, or produce, protein, portion.

The 28-year-old dietitian based in Los Angeles anchors her meals in protein, to help her feel full, and nutrient and fiber-packed produce, such as veggies and beans.

To portion her food, she takes a plate and fills about half with produce, about a quarter with protein, and high fibre carbs and maybe some healthy fats for the remainder, she said. PPP can be applied to any meal.

"That's kind of how I visualize my plate and then I reverse engineer my meals from that," Gorski told Business Insider.

She developed the simple template to help her clients who want to lose weight, because she noticed they would often fall into the trap of adopting an all-or-nothing mindset, which was tripping them up.

Clients thought "either I'm super healthy and I'm eating at home, or I'm dining out and eating fast food and junk food and more convenience foods, and I'm being 'unhealthy,'" Gorksi said.

"When you give people a template 'produce, protein portion,' it makes it a lot easier to find healthy options that align with your goals," she said.

Following this template helped Gorski lose 20 pounds in 2016, without cutting out her favorite foods.

"What's great about it is it helps you build the plate, but also helps you shift from the deprivation to the abundance mindset," Gorski said.

When it comes to weight loss, eating balanced, nutritious meals that don't feel restrictive is crucial to long-term success, she said.

PPP rule-approved meals Gorski eats on repeat:

High-fiber, high-protein pasta

Hailey Gorski

- High fiber pasta (portion)

- Ground beef in marinara sauce (protein)

- Three different frozen vegetables added into the sauce (produce)

Low-lift wraps

- High-fiber tortilla wrap (portion)

- Turkey slices (protein)

- Guacamole and arugula (produce)

Grain bowls

Hailey Gorski

- Grilled chicken (protein)

- Tomato, cucumber, red onion salad (produce)

- Wholegrain pita, hummus, olives (portion)

from Business Insider https://ift.tt/4zxuUrY

Friday, 20 March 2026

The 5 most important work relationships you should prioritize for career growth — besides your boss

Maskot/Getty Images

- Career growth depends on building a network rather than relying solely on your manager's support.

- Career coach Andrea Wasserman encourages forming cross-functional relationships to enhance visibility.

- Office "influencers" shape outcomes without formal authority, making them key allies for career progress.

Many corporate professionals believe their career trajectory hinges on one person: their boss. They think: If my manager advocates for me, I'll get promoted. If not, I'm stuck.

That's a misconception because promotions rarely come from a single champion — they come from a web of relationships. These include people who shape the perception of others, pressure-test your thinking, influence decision-makers, and speak about you when you're not in the room.

If you want your career trajectory to soar this year, you should be refining your relationship strategy, starting with these five categories of people.

1. The cross-functional partner who depends on you

High performers often invest in building deep credibility within their own team and spend significant time thinking about how to impress senior leaders, but neglect peers in adjacent functional areas. This limits visibility.

I once worked with a retail marketing director who consistently exceeded her revenue targets. She assumed that would be enough for promotion, but when senior executives evaluated her readiness for a broader role, they asked, "How does she lead cross-functionally?" Her merchandising partner on another team described her as territorial and protective. This stalled her progression.

She rebuilt the relationship by scheduling monthly alignment meetings with merchandising and supply chain, asking about their margin pressures, and proactively adjusting campaign timing to reduce markdown risk. Within two quarters, her boss told her those partners started advocating for her "one company" mindset.

Cross-functional relationships create leverage because they expand who experiences your leadership. Your reputation can't grow within your silo.

2. The culture carrier

Every organization has culture carriers who are respected insiders without an HR title or the formal authority to lead culture, who set an example of acceptable norms and embody how decisions actually get made. They may not have the biggest titles, but they have credibility and context.

When a newly promoted vice president entered a financial services firm, I saw him struggle in executive meetings. His ideas were strong, but they didn't land. He later realized he was presenting a detailed analysis in a culture that valued decisive framing.

He built a relationship with a longtime chief of staff who was widely respected but rarely in the spotlight. She helped him understand the company's "operating language," which is how leaders structure arguments, how disagreement is expressed, and what signals executive readiness.

Within months, his presence shifted. He wasn't more competent than before, but he was better prepared to show up appropriately. It's critical to understand the unwritten rules so you can move inside them with greater ease.

3. The influencer without formal authority

There's often someone who shapes outcomes without owning the final vote. It may be a product manager, a program lead who briefs the executive team, or a person who controls the data that frames strategic decisions. These influencers control how far your work goes and what people think of it.

A senior operations leader once told me she was invisible in the prep work for big meetings, even though she felt she had valuable contributions to make. Instead of chasing her boss and pleading for airtime, she focused on the strategy lead, who oversaw the synthesis of updates and recommendations from various functional areas. She began sending structured summaries — three risks, three opportunities, and one recommendation — to that person ahead of key meetings. Within weeks, her language began appearing verbatim in board decks.

Rather than demanding visibility, she became indispensable to someone who already had a seat at the table. While it's tempting to chase senior leaders, don't overlook the people who shape what those leaders see.

4. The truth-teller

Feedback can be hard to get. Your boss may soften it, peers may avoid it, and direct reports may filter it, but without it, your growth will stall. You need one person who will tell you the hard truths before they cost you credibility.

A high-potential director once asked a peer she trusted, "What's one thing I do that might be hurting how I'm perceived?" The answer she got made her uncomfortable: "You over-explain when you're presenting, and it makes you sound defensive." In executive settings, brevity signals confidence, but her error never came up in a performance review.

She began practicing tighter framing. Within months, leaders described her as more decisive and executive. The issue wasn't competence — she was simply unaware of a change she needed to make.

5. The sponsor — but built through exposure, not "pick your brain" requests

Senior sponsorship doesn't start with a formal ask for mentorship or coffee dates. It happens through consistent exposure to your work and your thinking behind it.

One client assumed his boss's boss would naturally champion him, having heard through the grapevine about his analytical rigor. He delivered strong results but only showed the output, not the problem-solving process. I coached him to shift his approach and, instead of presenting only one conclusion, bring structured options: "Here are three paths, here's the tradeoff, and here's my recommendation."

The goal is to have someone who references your strategic ability in executive meetings, so you become known as "already operating at the next level."

Next steps

If you're new to your organization, introverted, or stretched thin, prioritizing several relationships may feel overwhelming. It doesn't have to be.

Start with two relationships this quarter. Replace one transactional update with a strategic conversation. Ask one person for candid feedback. Offer one cross-functional assist that wasn't required. In a hybrid work environment, it's ideal to schedule these conversations for in-person days, but it's better to make them happen remotely than not at all.

If you focus only on impressing your boss, you narrow your sphere of influence. By building these five relationships, you expand your reach. This road map will ensure that enough of the right people experience your capabilities.

from Business Insider https://ift.tt/RUHw5ln

These 6 airlines offer beds in economy, with prices ranging from $150 to $2,600. Here's how to book them.

The "Relax Row" will give coach travelers a glimpse into what flying business class feels like. Patrick T. Fallon / AFP Air N...

-

The Bell V-280 Valor was selected as the Army's future long-range assault aircraft in 2022. Photo courtesy of Bell The US Army desi...

-

Big Tech is emerging a winner in the new H-1B system, while early-stage startups could lose out. Matthias Balk/nirat/Getty/Getty Images ...

-

Student-loan borrowers said they're worried about higher payments without the SAVE plan. Aaron Hawkins/Getty Images/iStockphoto Tru...